Oxstones Investment Club™

Oxstones Investment Club™By Macromon, Global Macro Monitor,

We here lots of talk these days about, Why Donald Trump’s Market Rally Echoes Ronald Reagan’s.

We are big fans of Chaos Theory,

Chaos theory is a branch of mathematics focused on the behavior of dynamical systems that are highly sensitive to initial conditions—a response popularly referred to as the butterfly effect.[1] Small differences in initial conditions (such as those due to rounding errors in numerical computation) yield widely diverging outcomes for such dynamical systems, rendering long-term prediction of their behavior impossible in general.

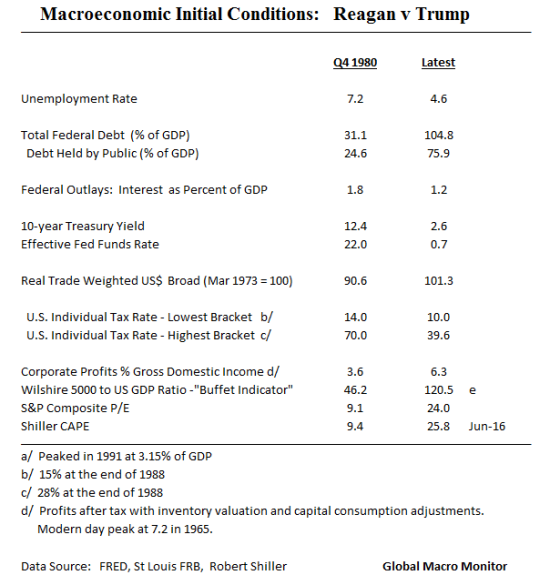

So we thought we’d take a look at the macroeconomic initial conditions at the start of the Reagan Presidency versus the incoming Trump Presidency.

Check out the data:

In all most all macro categories that we have have researched here, the initial conditions just aren’t their for a Reagan type bull market, in our opinion. First, and foremost, are the monetary headwinds.

Monetary Conditions

Reagan began his Presidency with interest rates nowhere to go but south. A 22 percent Fed Funds rate and a 10-year Treasury yield of 12 1/2 percent. Though interest rates were the not the policy target of the Fed at the time, just several months into the Reagan Presidency the 35-year bond bull market ignited and drove almost all asset prices from real estate to stocks.

The polar opposite monetary conditions exist at the advent of the Trump Presidency. Interest rates have nowhere to go but north, we believe, especially if Mr. Trump’s fiscal policy is implemented.

Unemployment

Mr. Trump will not have the labor slack and surplus to draw upon to drive economic growth. The country is pretty much at full employment. This risks much higher inflation than anticipated if his policies are passed and thus a more aggressive Fed.

Total Debt

President Reagan began his Presidency with a relatively small stock of debt. Mr. Trump will inherit a debt-to-GDP ratio almost three times that of President Reagan. This leaves less room for deficits, as a result of his tax cuts and increased spending. The Trump plan is to increase economic growth and thus tax revenues through supply side and micro and regulatory policy. This is the second chance for this argument to succeed. Watch this space.

The high debt stock risks a spike real interest rates.

Real Oil Price

President Reagan took office with a relatively high real oil price. Note this was in an era when high oil prices were considered “bad” for the economy. The real oil price dropped almost 75 percent in the first five years of the Reagan administration. President Trump will inherit a real oil price half that of Mr. Reagan, coupled with the ambiguity of not knowing if higher oil prices are good or bad for the economy. Don’t know what to do with this one.

Dollar

Mr. Trump inherits a real trade weighted dollar a little over 10 percent stronger than President Reagan and, most likely, headed north given the world divergences in growth and monetary policy. This could act as headwind on corporate profits and export growth.

Individual Tax Rates

This is the pearl and central to the supply side argument. Cutting marginal tax rates to incentivize economic behavior and growth, which will increase tax revenues that offset the revenue loss from the tax cuts. Note, President Reagan cut the top rate from 70 percent to 28 percent. That was Yuuuge! Mr. Trump just doesn’t have the room to do such large tax cuts as he starts at a lower base with the highest tax rate at around 40 percent.

Corporate Profit Margins

President Reagan took office with a lot of corporate inefficiency and room to expand corporate profits. It feels we are close to peak margins. Didn’t we just have an election to improve the wages of the average worker? Stay tuned.

Stock Valuations

Much like the debt stock, Mr. Trump will inherit a stock market that is relatively highly valued. Note, one of Warren Buffet’s stock market valuation metrics, Stock Market Cap to GDP, is more than 160 percent now than it was when President Reagan took office. The U.S. will need lots of economic growth to “grow” into this metric.

Conclusion

There you have it. The macroeconomic initial conditions at the beginning of two Presidencies. And this is just our first whack at this type of exercise.

President Trump is going to have to depend on “animal spirits” to do a lot of the heavy lifting and an exquisite execution of supply side, microeconomic, and regulatory reform to increase potential GDP growth. Higher growth will increase the top line of companies and improve earnings.

Can we rally a lot? Absolutely. A Reagan bull market? We don’t think so. Could be wrong.

Stay tuned.

http://wp.me/p14UId-8IS

Tags: buffett indicator, Corporate profit margins, Donald Trump's market rally, market valuation comparisons in the 1980's to 2016 conditions, market valuations, Oil prices, Schiller CAPE, Stock Market Cap to GDP, Trump presidency's macroeconomic conditions vs Reagan presidency's macroeconomic conditions, U.S. 10 Yr Treasury Yields, U.S. debt to gdp ratio, U.S. dollar, U.S. interest rates, U.S. monetary conditions, U.S. tax rates