Oxstones Investment Club™

Oxstones Investment Club™From www. ciovaccocapital.com site,

If you are involved in the financial markets in any way, shape, form, or fashion, you know Europe is what matters right now. When the Financial Times caused a buying panic on October 4 after reporting European Union finance ministers are looking into ways to coordinate recapitalizations of financial institutions, it highlighted the market’s hope for a quick resolution to the European debt crisis. Before we review some common misconceptions about realistic timetables in Europe, our main themes are summarized in the excerpts below from an October 4 Bloomberg article:

German Chancellor Angela Merkel stiffened her resistance to joint euro-area bond sales, saying that investors yearning for a single gesture that can end Europe’s sovereign debt crisis now will be disappointed.

The euro area has to resolve “that the time of living above our means is over once and for all” and pursue debt reduction that will stretch over “many years,” Merkel said in a speech to members of her Christian Democratic Union late yesterday in Magdeburg, eastern Germany.

She said that issuance of shared debt by euro countries isn’t the solution to the problem spilling from Greece, even though some may long for the “big bang” to end the debt crisis. “Whoever believes that has no clue about the economy,” she said.

Financial markets are always looking ahead to the next milestone or “fix” in Europe. Below we explore what appear to be disconnects between what investors hope will happen and what is actually happening:

A euro area bank recapitalization program will be announced within days – right? Let’s go right to the source – below are some phrases and excerpts from the Financial Times article that caused such a bullish stir in the financial markets – as you read them ask yourself if a plan appears to be in place or if an announcement is imminent with specifics:

European Union finance ministers are examining ways…

Although the details of the plan are still under discussion…

“This should be regarded as an integral part…”

“It’s clear now that the European banking system needs to be strengthened…”

Finance ministers agreed on the need to act through national capitals while co-coordinating their approach.

A first step would likely be to ensure all countries have mechanisms in place..

There was “no formal” decision to begin a Europe-wide effort…

Finance ministers left open the exact means of how recapitalization would be coordinated.

One option being examined is to set new higher capital requirement for banks.

Think about that last line above – so, they mean the banks will be required to raise more capital?…In the public markets? In the words of John McEnroe, “You can’t be serious!”

In a recent CNBC interview, Nick Parsons of National Australia Bank hints that formal recapitalization of banks may not occur for some time.

“We can have an orderly default. Greek’s defaults on its debt, it does not leave the single currencies. So Greece remains very firmly within the eurozone. When European banks have to recognize the hit in terms of money lost on loans to Greece, then countries national governments in Germany, France and elsewhere will be forced to recapitalize their banks and they will be forced to create a much more stable rules based monetary union. But it’s not until Greece default that politicians will actually come together and put those measures in place. For the moment, they are in that awful position of just denying what the rest of the world sees both inevitable and obvious.”

An announcement concerning the use of leverage in the European Financial Stability Facility (EFSF) is just around the corner – right? The EFSF will be leveraged only if all countries sign off on it. From German newspaper Spiegel:

Even as the European Financial Stability Facility (EFSF) is now being boosted to increase its lending capacity to €440 billion, many say that won’t be enough and are calling for yet another expansion of the fund, though leaders in Berlin have firmly rejected such a course of action.

From the CNBC interview with Nick Parsons:

“No, I don’t think the EFSF will be leveraged because the German politicians, who last Thursday voted for the EFSF, voted for it on the basis that this was as it was discussed on the July 31 leaders meeting in Brussels. Many of the German politicians who went through the yes vote said, yes but no further and they made it very clear that they would be voting against further leverage. That leverage itself has got to be unanimous so I don’t think we will end up with a leveraged EFSF.”

Another perspective on leveraging from Germany’s Spiegel:

Indeed, European officials are already discussing ways to either boost the fund yet again or to leverage it, using the fund’s assets as collateral to borrow up to €2 trillion. On Tuesday, Belgian Finance Minister, at a euro-zone meeting of finance ministers in Luxembourg to discuss the crisis, said that the euro-zone is likely to pursue ways to boost the fund. That, though, is not a foregone conclusion. Germans in particular have been extremely wary of throwing additional billions at the debt crisis and a parliamentary vote last week to expand the EFSF to its current level already cost Chancellor Angela Merkel significant political capital. Several politicians from within her ruling coalition have said that further expansions are out of the question.

The markets hope the European Central Bank (ECB) will step up to the leverage plate. Reuters reported on October 3:

Jean-Claude Juncker, the chairman of the Eurogroup ministers, said the European Central Bank was not the main avenue being explored to increase the firepower of the European Financial Stability Facility, an acknowledgement that is likely to undermine confidence that the bailout fund can be sufficiently scaled up to calm febrile financial markets.

Other problems with leveraging the EFSF, as outlined by the Wall Street Journal, include:

The EFSF portfolio would be chock-full of undesirable bonds–precisely those that financial institutions didn’t want to buy in the first place–so it wouldn’t be the best collateral.

The scheme relies on the private sector to lend to the EFSF in times of trouble. But that’s precisely when the private sector is least likely to be lending.

It won’t come as cheap as ECB financing, or as cheap as the EFSF’s own triple-A bond market funding.

Banks would be wary about large commitments to a leveraged EFSF. The EFSF is an off-balance-sheet vehicle. Its creditors have no recourse beyond the guarantees that the euro-zone countries pledge to it.

The markets are stabilizing since action is being taken in Europe – right?: The Wall Street Journal reported on October 4:

The two-year swap spread, a closely watched gauge of credit-market risk, keeps blowing out and now trades at the widest level since June 2010.Growing worries about counterparty risks — especially involving banks exposed to Greek government bonds, such as Dexia — could spell more problems for eurozone banks, sending their funding costs even higher.

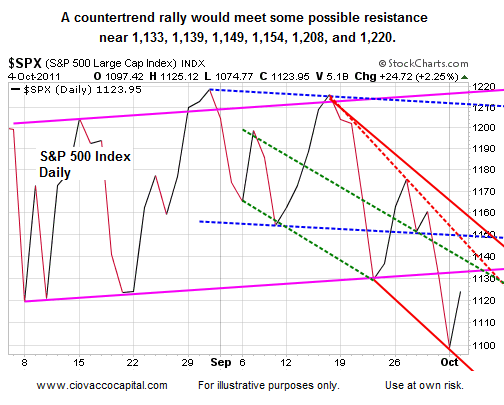

As conditions change and pressure mounts on policymakers, the markets may get some of their prayers answered. However, the current state of affairs points to more disappointments and delays from euroland. Consequently, we will still give the bear market the benefit of the doubt by sticking with bonds (TLT), the U.S. dollar (UUP), and S&P 500 shorts (SH). Bear markets often experience hope-and-rumor-induced rallies that share a common trait – they are retraced 100% on the next leg down. As we outlined on September 22, the S&P 500 will most likely see a close below 1050 sometime in the coming weeks. Could the markets rally sharply for a time and remain within the bounds of that probabilistic forecast? Sure – possible areas where sellers may become active again are shown below.

Just as Americans got a case of bailout fatigue, taxpayers in Germany are firmly opposed to any more bailouts or leveraging. Can you imagine if the U.S. government announced another bailout for Bank of America or Morgan Stanley? As noted by German Chancellor Merkel, Europe is faced with debt reduction that will stretch over “many years,” not a matter of days, weeks, or months. Danny John, of the Sydney Morning Herald, provided us with a tidy close on October 4:

For those optimistic investors hoping for a quick resolution to the debt crisis in Europe, which may bring some much-needed calm to financial markets, there is little doubt they are in for a long wait. We are not talking weeks here.

Tags: bank recap, big picture, ECB, EFSF, EU, EU Banks, Germany, Western Europe