Oxstones Investment Club™

Oxstones Investment Club™by Peter Nielsen

of Saturna Capital

Encouraging fundamentals and positive developments in broadly-used sector classifications and US tax structure bode well for Real Estate in 2016.

Real Estate has come of age and will be moving out on its own this summer, leaving its parent sector home of Financials to reside in its own self-titled headline sector. We foresee positive developments and a few risks for this asset class as a result of this and other significant factors converging on the industry.

What are the drivers for 2016?

GICS to add Real Estate as a separate sector

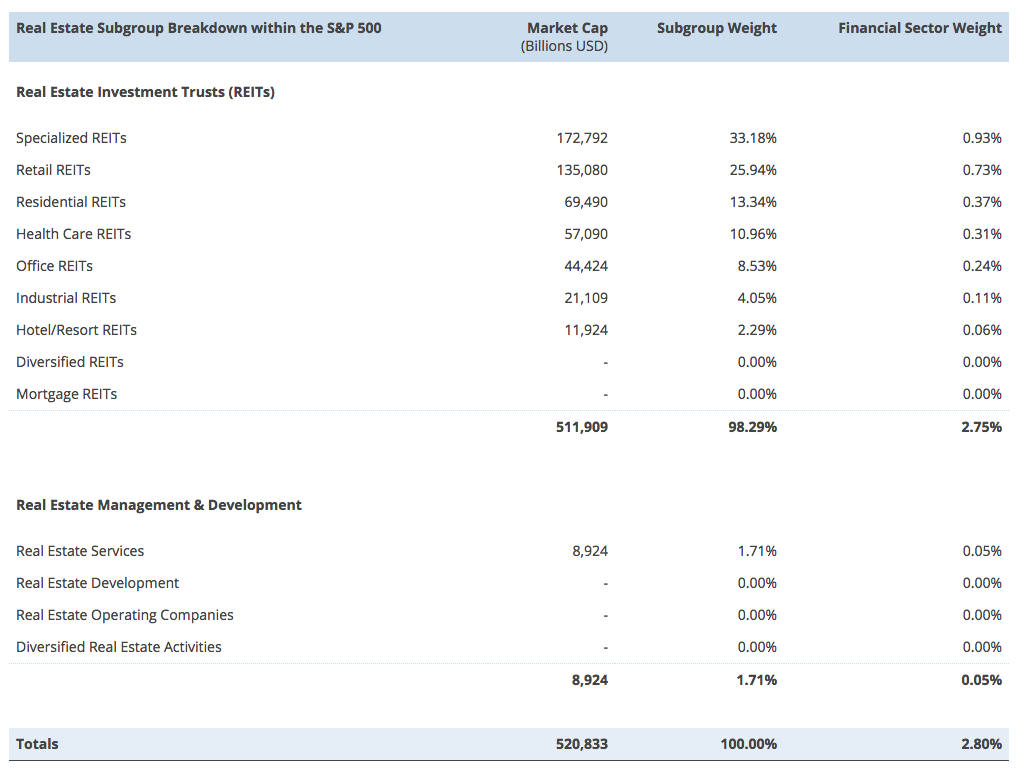

The Global Industry Classification Standard (GICS) Committee announced last year that it will add Real Estate as an eleventh, distinct sector in August 2016, which in turn will impact the S&P and MSCI indices. As the first new sector added since the GICS system was created in 1999, Real Estate will include Equity Real Estate Investment Trusts (REITS) while Mortgage REITS will remain under Financials. Currently, the Financials sector as a whole comprises about 16% of the S&P 500 Index. The Real Estate subgroup constitutes 3% of the index and 18% of the overall weight within the Financials Sector.

REITs will dominate the new Real Estate sector with Specialized REITs having the biggest weight (assuming no change to this classification scheme). Retail, Residential, and Health Care REITs also carry double-digit weights. It is worth noting that non-REIT real estate segments are a component of the sector though they are not currently captured by the S&P 500.

Investors may wonder whether a dedicated Real Estate sector will draw more capital into REITs. Many (if not most) institutional investors use the S&P 500 as their de facto sector allocation standard, and Financials exposure varies greatly between investors. Investors who gain exposure to the sector may be somewhat indifferent to industry weights within the sector. With increased visibility of Real Estate comes the likelihood of some risk exposure rebalancing that will favor REITs.

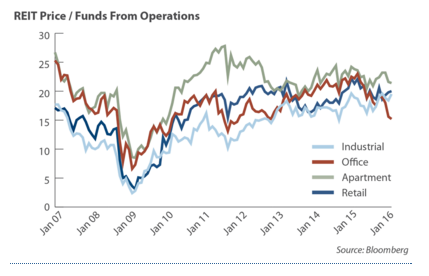

The popularity of REITs derives from their income and liquidity. Given their interest rate sensitivity, REIT valuations not surprisingly rose along with post-financial crisis expansionary monetary policy. Ratios of REIT prices versus their funds from operations (FFO) currently sit close to pre-crisis levels.

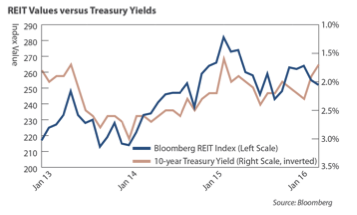

Spreads of real estate yields to Treasury bonds remained tight though relatively stable over the last two years. Indeed, property-level fundamentals continue to be encouraging. All real estate subsectors are experiencing an upturn in rental income growth and managers appear to be doing a good job of managing their portfolios.

Tax code changes encourage foreign direct investment in US real estate

The Foreign Investment in Real Property Tax Act (FIRPTA) enacted in 1980 set up a tax foreign investors must pay on realized gains from US property transactions. FIRPTA changes signed into law in late 2015 are expected to ease the chilling effect of the tax on foreign direct investment in real estate. Foreign pension funds, which have been effectively absent from the US real estate market, will now enjoy a level playing field with US pension funds, qualifying for the same waiver of the tax imposed under the Act. The changes to FIRPTA include:

- Foreign pension funds’ exemption from FIRPTA taxation when investing in US real estate via direct investment, partnerships, and private equity pools

- An increase in tax-exempt REIT ownership to 10% (from 5%) for foreign pension funds

In 2015, foreign pension funds invested $7.5 billion in US real estate amounting to about 10% of total foreign investment. More capital seeking assets is likely to have positive effects on liquidity and will present a welcome change for REITs given their soft performance in front of the recent Fed rate hike.

REIT fundamentals remain positive

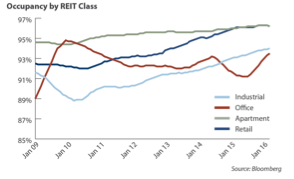

Real estate assets continue to benefit from an improving economy. Real estate will always remain a factor of production, and falling unemployment has provided key support for values across the country by contributing to rising absorption rates — the rates at which available properties are sold from market inventory. The evidence of improving demand is fairly broad-based, and many operators report occupancy rates over 90%. With rents rising and vacancies falling, what’s not to like? Fundamentals remain encouraging despite a few warning signs (more on that below).

REITs often have deep development pipelines

One constant theme from the REIT industry over the last several quarters has been the growing bias toward build versus buy. With the rates of return on real estate investments low and private market values high, REITs use internal development programs to increase yield on capital. With rare exception, commercial real estate services firm CBRE Group sees continued downward pressure on returns for 2016.

Development programs require multiple years to execute. Late 2011 increases in project development values have led to an early 2016 surge in properties put into use. With existing occupancy levels at a high point, REIT earnings should grow faster than in 2015 if absorption trends hold and assuming all else held constant. It seems the build versus buy theme will continue for some time as many REIT operators report lower rates of return outside the REIT structure than inside, providing an avenue for increasing returns on capital. We see little indication that new supply is diluting rental growth.

What are the downside risks?

Interest rates

A well recognized inverse relationship between long-dated Treasury yields and REIT prices exists, with falling yields tending to lift REIT valuations. REIT valuations softened in front of the most recent Federal Open Market Committee meeting illustrating investor concern over how rising rates may affect the sector.

Consensus estimates have the US 10-year Treasury yield rising to 2.39% from its current 1.83% by the end of 2016 (+56 basis points).

High occupancy rates, the ability to raise rents, good expense management, and internal development all result in one thing: growth in FFO. Rising FFO yields suggest market concern about rising Treasury yields as spreads have widened.

Are we late into the Real Estate cycle?

This is the proverbial “million-dollar question.” Some REITs have reported retailer sales slowdowns and store closings. These tend to be outside of the regional mall space (local strip malls and malls in secondary urban markets). Boston Properties reported a slowdown in technology hiring, and this is starting to be felt in demand for office space. Some REIT operators may share a fear of a slowdown (whatever that looks like). One retail REIT we follow appears to be increasing the sales breakpoint on new leases. This effectively lowers the REIT’s risk exposure to tenant sales trends while conceding some of the upside.

Other REITs are paring back exposures to perceived vulnerable markets. One Midwest-oriented REIT is actively selling small-market urban office buildings, allowing the REIT to reduce leverage.

Real estate services firm Jones Lang LaSalle does not view the real estate cycle as late-stage. They continue to see gains in capital value across most major markets, though for many markets capital appreciation is slowing.

CONCLUSION

Real Estate fundamentals remain encouraging, despite many markets experiencing slowing growth in capital values. REIT operators appear to be taking steps to manage risk. As foreign pension funds seek out investment opportunities that were formerly not available to them, the potential for increased liquidity will help support asset prices. Add in the sector classification change undertaken by Standard & Poor’s and it becomes difficult to get too negative on real estate.

Copyright 2016 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 10 · No. 2

Important Disclaimers and Disclosures

Performance data quoted represents past performance which is no guarantee of future results.

This publication should not be considered investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor’s circumstances or otherwise constitutes a personal recommendation to any investor. This material does not form an adequate basis for any investment decision by any reader and Saturna may not have taken any steps to ensure that the securities referred to in this publication are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the publication.

The information in this publication was obtained from sources Saturna believes to be reliable and accurate at the time of publication.

All material presented in this publication, unless specifically indicated otherwise, is under copyright to Saturna. No part of this publication may be altered in any way, copied, or distributed without the prior express written permission of Saturna.

The S&P 500 is an index comprised of 500 widely held common stocks considered to be representative of the US stock market in general.

The Bloomberg REIT Index is a capitalization-weighted index of Real Estate Investment Trusts have a market capitalization of $15 million or greater.

As of 12/31/2015, no Saturna Fund own shares in CBRE Group (CBRE), Boston Properties (BPX), or Jones Lang LaSalle (JLL).

http://www.advisorperspectives.com/commentaries/20160407-saturna-capital-2016-commercial-real-estate-outlook

Tags: asset class, foreign pension funds, Global Industry Classification Standard, Institutional Investors, real estate, real estate fundamentals, real estate investments, REITS