Oxstones Investment Club™

Oxstones Investment Club™By Tim Hanson,

If you’re an investor, then you know about margin of safety. Pioneered by value investor Ben Graham and carried on by the likes of Warren Buffett, it’s the idea that you should buy an asset for less than your estimate of its worth in order to earn higher returns and account for the possibility that your estimate might be wrong.

Conventional wisdom suggests that the greater the margin of safety, or the lower the market price relative to the fair value estimate, the better the opportunity.

How that worked and why it no longer does

In his seminal work The Intelligent Investor, Graham writes about Northern Pacific Railway common stock. He explains that the company’s earnings are understated by accounting rules because they do not include the earnings from another railroad, C.,B. & Q., of which Northern Pacific owned a little less than 50% (Northern Pacific would include the earnings if it owned more than 50%). According to Graham, adding in its share C.,B. & Q.’s earnings would increase its earnings from the reported value of $3.80 per share to $6.20 per share. Add in a few other lesser-known profit centers and Northern Pacific’s true earnings were actually $7.15 per share. Put that against a $16 stock price and you have a stable railroad trading for less than three times earnings. Further, by restraining its dividend during this time period, Graham contends that Northern Pacific effectively hid its true earnings from investors while stockpiling equity on its balance sheet.

If only it were still that easy.

Graham lived in a different time. He lived before before Reg FD, before the Internet, and before hundreds of thousands of people and hundreds of thousands more algorithms were trolling the market in search of excess return. He lived, in other words, in a time of greater information asymmetry — when it was possible to hit upon a truth of which the rest of the market was not yet aware.

Today, however, U.S. companies must disclose information to all investors at the same time, anyone can access the world’s knowledge in an instant, and computers are laying waste to pockets of inefficiency. The market, for example, sussed out the value of Alibaba Group and its value to Yahoo! shareholders long before Yahoo! even ever did — though given that management team’s dearth of bright ideas, perhaps that’s not saying much. And today investors arguably prefer companies that don’t pay dividends, believing that capital should more profitably and more tax efficiently be reinvested in growth opportunities or used to repurchase shares.

Hope springs eternal

Yet if you read financial reports, professional investors consistently tout liquid stocks trading for 40% to 50% or more below fair value. This is delusional.

Valuing an asset is difficult and identifying an undervalued one even more so. Even in Graham’s heyday, most investors did not beat the market. And today more than 90% of professional money managers fail to best their benchmark. This suggests that there are not as many good ideas as the financial industry says there are.

What’s more, the search for margin of safety has given rise to its inverse: the margin of danger. This is the notion that by concentrating capital in the ideas they perceive to be the most undervalued, investors may actually be making themselves worse off.

Making room for error

As the market gets smarter, its prices get more accurate. As market prices get more accurate, investors who think they have found stocks trading for significantly less than fair value have likely not uncovered true bargains. Rather, these investors are more likely to have made a mistake, miscalculated, or failed to account for a risk factor that is apparent to the rest of the world.

By buying into these perceived bargains, investors are thus investing in ideas they either don’t know how to analyze or don’t know much about. This is the definition of dumb money, and what makes this brand of dumb money dangerous is that it does not realize how dumb it is. It’s dumb money masquerading as smart money. And as for the returns that will come from that, they are at best random and at worst catastrophic since the investor in question — wrong from the outset — is ill-equipped to make accurate future decisions about that stock.

The problem with predictions

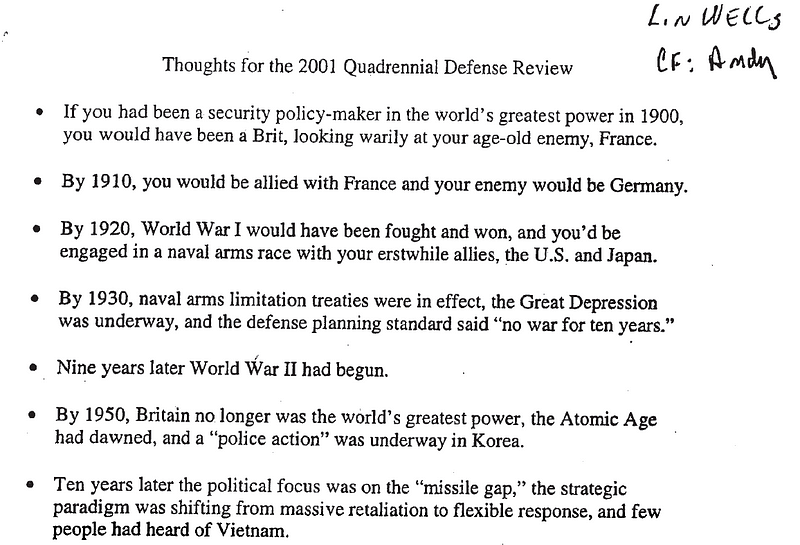

Back in 2001, then Secretary of Defense Donald Rumsfeld forwarded along a memo to then President George W. Bush from an analyst at the Pentagon named Lin Wells. Its contents were some musings on the upcoming Quadrennial Defense Review — a process our government undertakes every four years to try to identify the threats of the future and put in place a long-term plan to manage them.

In a world of budget mismanagement, pork barrel politics, and never-ending election cycles, this sounds like exactly the kind of longer-term strategic thinking we deserve from our government. It sounds like the kind of process that would make us safer.

But Wells warned against putting too much stock in the exercise, citing significant geopolitical developments going back the past century that had seemed inconceivable just a decade prior.

He noted, for example, that by 1930 “the defense planning standard said ‘no war for 10 years’…Nine years later World War II had begun.” He concludes by remarking that while he was not sure what 2010 would look like, “it will be very little like we expect, so we should plan accordingly.”

This is sage advice. If we cannot accurately predict the future, then the more assuredly we act on our predictions, the more dangerous we make the world around us. For example, if the government had concluded back in 2001 that the only threat to our security was a war with China, then we’d have focused on training intelligence analysts to speak the various Chinese dialects, increasing our supply of long-range missiles, and ordering up intimidating aircraft carriers. And if this was all we did, it would have left us even more unprepared to manage an Arabic-speaking, non-State terrorist threat.

Similarly, in investing, one popular risk management exercise is the premortem. This is an exercise in which one assumes a stock that one has purchased has declined some magnitude from the purchase price, with the analyst then tasked to explain how this could have happened. Its goal is for an otherwise bullish analyst to be forced to contemplate risk factors that went unforeseen or unappreciated during the initial analysis.

But like the Quadrennial Defense Review, my experience is that premortems are far less useful than they sound like they would be. It’s difficult to predict big changes — and particularly big, bad changes. If our well-heeled Department of Defense, with its $600 billion annual budget, access to global intelligence networks, and decades of experience can’t do it, what hope do the rest of us have? What’s more, if they could, they wouldn’t act opposite that assessment. For investors, it’s the same. You probably can’t see the Sword of Damocles hanging over your best idea and if you could, then it probably wouldn’t be your best idea.

Undervalued, or a long shot?

All of this is to say that if you’re an investor who has found a stock trading for 50% of fair value, your next action should not be to buy the stock, but to check your work. Market prices are being discovered by an ever-wiser consensus, and the more your answer deviates from that consensus opinion, the more likely you are to have made a mistake in your analysis. This could be as simple as linking the wrong cells in a spreadsheet to failing to contemplate currency risk to not questioning a baseline assumption (all mistakes I will cop to having made at one time or another).

For example, back in March 2015 the three most “undervalued” stocks identified by the investing team I worked on were Geospace Technologies, a Houston-based company that sells seismic equipment to the energy industry, Monitise, a U.K.-based company that builds mobile payment technologies, and Denbury Resources, an unconventional oil and gas producer. These names were allegedly trading for 40%, 70%, and 50% of our estimates of fair value, respectively. Yet since that time these stocks are down 13%, 87%, and 65%, respectively, while the market is up a little more than 2%.

What’s more, these undervalued names turned out to be among the worst performers in our universe.

Does that make us bad investors? It would, if we had invested and rebalanced rotely into the names we perceived to be the most undervalued. Instead, those significant discrepancies between our valuations and the market valuations raised questions. In the cases of Geospace and Denbury, were we too optimistic about a rebound in oil prices and therefore the health of the energy industry? In the case of Monitise, had we overestimated the value of its technology after Visa, a key shareholder, opted to sell its stake? We weren’t sure at the time and therefore did not act aggressively.

As it turns out, the answers to those questions appear to be yes and yes. (Incidentally, the fourth-most undervalued name was Horsehead Holding, a one-time favorite of noted value investor Mohnish Pabrai, which has since declared bankruptcy.)

Coping mechanisms

This isn’t to say that there aren’t thousands of stocks trading for 50% of a potential future price. For example, hundreds of names in the energy sector will likely more than double if oil prices return to $100 per barrel. But that’s not margin of safety. Rather, that’s a potential outcome in a specific scenario — not the fair value of the stock. It’s important to recognize that difference. It’s the equivalent of betting on the race horse with the longest odds and thinking that’s a bargain because every horse running has the same chance of winning the race.

Having said that, I continue to believe that small pockets of inefficiency do exist in the stock market even if identifying them has gotten more difficult, more complicated, and more dangerous. To find them, some rules of thumb can be helpful.

Rules of thumb are, of course, crude and simple, which is precisely why they are effective in managing complicated situations. If you’re lost, stop moving. Whether you’re really lost or just a little lost, you can then figure out where you are, ask for assistance, or wait for help. What you won’t do is make the situation worse. If, on the other hand, you’re really lost, but act as though you’re just a little lost, chances are you’ll just get more lost.

When it comes to investing, I don’t take a position size larger than the number of years I’ve followed a company. One year, no more than 1%. Five years, no more than 5%. This limits my exposure to having made a mistake in analyzing the companies I’m most likely to have made a mistake in analyzing — the companies I am only just beginning to get to know.

Similarly, I now start my research work not with the companies that I estimate to be very undervalued, but rather with the companies I estimate to be slightly overvalued. If the consensus is that these companies are better than I think they are, then chances are that I am missing a key strength of the company. And if most people are thinking like me, then it may be the case that the consensus is actually underestimating the long-term value of that key strength.

This is the Facebook story of the past few years. The stock seemed overvalued at its IPO because of a lack of earnings, but the market awarded it a premium valuation because of the strength of its network effect. Yet even the most ardent believers in the strength of that network effect underestimated the profit stream it would produce.

Finally, whenever I update a valuation or analysis, I save it anew rather than overwrite what was there before. This enables me to go back see what I thought before I learned something new. When I’m consistently surprised — either pleasantly or unpleasantly — I take it as a sign that I may not know what I’m talking about.

Regardless of how you choose to account for your margin of danger, it can be humbling to accept that the more strongly you believe in a non-consensus idea, the more likely you are wrong. There’s always the chance you’re right, of course, and great progress and profits are reaped when iconoclasts are vindicated, but go slow and check your work. It’s always important to be deliberate and thorough and account for uncertainty, but especially so when the odds are not in your favor.

https://medium.com/@timhanso/margin-of-danger-6a2431b3068e#.j73te4ass

Tags: ben graham, investing philosophy, investment wisdom, Margin of Safety, market efficiency, position sizing, risk management lessons, Warren Buffett, world of information efficiency