Oxstones Investment Club™

Oxstones Investment Club™One of the most influential business op-eds of the decade was Marc Andreessen’s August 20th, 2011 piece in the Wall Street Journal entitled, “Why Software is Eating the World.” It was written during a period where business/economic people were still focused on the financial crisis, while European government debt was imploding, and while the US Congress was contemplating defaulting on the national debt. Not many people were focused on tech.

Fast forward 5 years, and “software is eating the world” and “disruption” have become business/tech gospel akin to expressions from the late ‘90s like “new paradigm.” Over that time period the stocks of Apple and Microsoft are up over 100%, Google and Netflix 200%, Amazon 300%, Tesla 800%, and Facebook IPO’ed to become a $300 billion company. Uber has a private market valuation of over $60 billion. The combined market caps of those 7 companies is over $2.3 trillion. Collectively they still have much growth ahead of them, but from a business power standpoint these companies have become like Wal-Mart and GE in the 1990′s, and they’re best thought of as incumbent titans rather than small upstarts with a large greenfield in front of them. Regulators have begun kicking the tires on the business practices of most of these companies. Even “Twitter eggs” are talking with confidence about self-driving cars and drones and virtual reality. Marc should declare victory.

The bigger business story over the next 5 years is going to be a capacity-constrained US economy where the housing sector is taking “inputs” like labor and capital from all other sectors. Ergo, housing is set to eat the US economy.

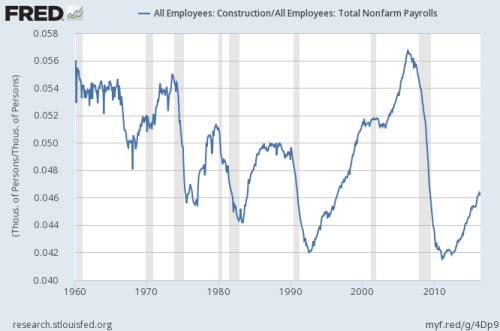

One way to show how much more growth housing, and construction more generally, has in front of us is to look at construction’s share of total employment. It’s currently 4.6%, and in every cycle ever it’s gotten to at least 5%. Given 1) the size and hence housing needs of the Millennial generation in years to come, 2) the lack of construction, of single family especially, since the financial crisis, 3) the potential for infrastructure spending from the next president, whether it’s the Hillary/Dem version or the Trump “build a wall” version, 5% seems like a reasonable conservative target for how high this will go over the next 3-5 years.

At a current total employment level of 143.9 million people (establishment survey), this means we need an additional 550,000-600,000 construction workers.

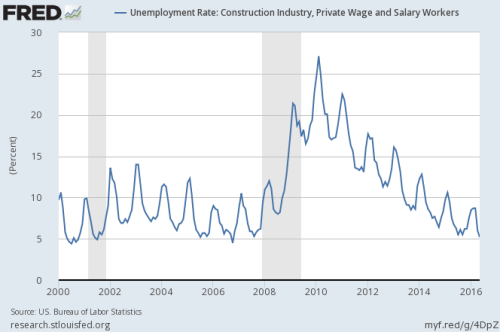

This is a problem because we’re already near record lows for construction unemployment:

How are we going to find them? 87-88% of construction workers are men, a ratio that hasn’t changed in 25 years. So we’re largely talking about men that we need.

I’ll also make the assumption that the missing male construction workers are going to be under the age of 55. Maybe it’s a bad assumption, feel free to correct me. But anyway, here’s a chart of unemployed men under the age of 55:

There are currently 3.3 million unemployed men under the age of 55. The low in the last cycle was 3.2 million in Q3 2006. In the late ‘90s it was around 2.6 million, so that provides more hope. However, the late ‘90s labor force was generally younger and less educated than today, making the pool of potential construction workers arguably larger than it is today.

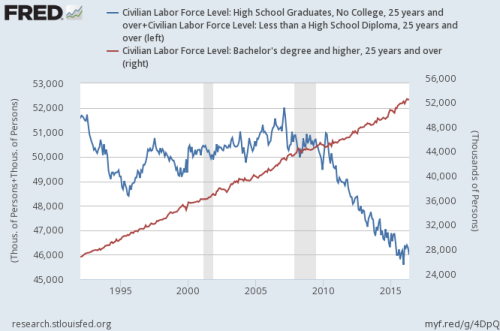

The educational composition of the labor force has changed in a dramatic way over the past 20-25 years. Since 1992, the number of college grads in the labor force has gone up by 25.8 million while the number of workers with a high school degree or less has fallen by 5.5 million.

Putting it all together:

-The economic shortfall in the US right now is mostly on the housing side. Because of how important housing is to the US economy, this is why 4.7% headline unemployment doesn’t feel like full employment.

-Construction employment as a share of total employment is likely going to rise at least another 0.4% to get to a level of 5% in this cycle.

-At the current level of employment, this means we need another 550,000-600,000 construction workers.

-Construction unemployment is already near record lows.

-Demographic trends in the US – an aging workforce, a workforce that’s growing more educated, the changing mix of immigration towards Asian knowledge workers rather than Hispanic blue collar workers (29% of construction workers are Hispanic) – all act as headwinds towards finding more construction workers.

-From a labor slack standpoint, the pool of potential construction workers is probably well-represented by unemployed men under the age of 55. To get back to late ‘90s levels of male unemployment (from a level standpoint, not an unemployment % standpoint), we would need essentially every single male unemployed worker who finds a job in the coming years to go into construction. This doesn’t take into account skill, desire, education level, geography, etc.

If we had to find 500,000 construction workers tomorrow, from a math standpoint it would be impossible. The slack isn’t there. But this isn’t the way things work in the real world. Time and market forces allow for adjustments. So here’s what that means:

-Over time, as construction employers become more aggressive they will bid away workers from similar fields – agriculture, oil & mining extraction, manufacturing. New entrants to goods-producing fields will be drawn overwhelming to construction, so as workers quit or retire from agriculture/oil/manufacturing-related industries it will create increasing scarcities in those industries.

-Goods-producing/blue collar workers will increasingly bleed from the Midwest/Northeast to the faster-growing southeast and west coast, where increasing numbers of construction jobs will be. This will put more and more of a strain on Midwest/Northeast goods-producing firms.

-With construction-friendly immigration flows not being what they were, the globalization solution will be to move ever more numbers of agricultural/manufacturing activity overseas to free up their domestic workers for construction. Neither California farm owners nor Midwest voters and governments will be happy about this.

-Construction wages/costs going up will mean higher housing/real estate costs for households and firms, leaving less of a spending pie available for the rest of the economy. If you’re spending an extra 3% of your pay on housing that’s taking business from a grocery store or a movie theater or Amazon.

-Capital will flow increasingly towards the housing sector, starving other sectors of capital. If construction can’t achieve productivity gains then labor shortages in other sectors (agriculture, manufacturing, entry level services/fast food) will mean more and more incentives to automate labor-intensive tasks to free up those workers to work in construction.

“Software eating the world” implied that digital upstarts were going to create low cost solutions to take demand away from older, high cost analog firms. Amazon eating big box stores, Facebook eating print and TV. Demand was going to shift. “Housing eating the US economy” implies that housing is going to steal your inputs. They’re coming for your workers and capital on the supply side. It’s a different dynamic but a similar outcome – housing is poised to reassert itself as the main driver of the US economy.

Tags: Amazon, Apple, blue collar workers, construction workers, facebook, financial crisis, Google, immigration flows, labor force, Microsoft, National Debt, netflix, Tesla, uber, us economy