Oxstones Investment Club™

Oxstones Investment Club™by H. Bradlee Perry

Experience is the best teacher. How true!

I have been a professional investment manager for 62 years, mainly at David L. Babson & Co., where I managed portfolios for all kinds of individual and institutional clients and then served as president and chairman of the firm for 26 years (while still managing clients’ accounts). Subsequently, I have been an independent investment consultant.

Through all this long period of managing investments and writing articles about the investment process (plus one book), I have accumulated a lot of knowledge that’s been invaluable to me and my clients. So now I’d like to pass on a few thoughts about key things I’ve learned from my many years of generally successful experience. Most of these will be familiar to my long-time readers and to AAII members who have heard my talks at national and local chapter meetings in past years, but the ideas are worth repeating.

Act on What You Know for Sure

Act on what you are certain about—not on what you’re guessing about or what you think might happen sometime later. Recognize that the future is largely unknown, so precise forecasts will be wrong at least as often as they are right. And even one bad misfire can damage a portfolio for a long time. So basing today’s decisions on uncertain forecasts and other sorts of guesses is truly dangerous. To paraphrase my favorite quotation from the sage of the ballpark, Yogi Berra, “We can’t predict the future because it hasn’t happened yet.”

This fact leads to my oft-repeated admonition: DO THE MATH. Numbers show us what is factually correct, what has happened in the past and what is happening now—what we do know. They provide an essential discipline for our thinking, so use them as a key input in all your conclusions—ones about the economic background, the status of financial markets, the fundamental position of various companies, and especially about the valuation of shares.

In this respect, I have a high regard for Martin Wolf, the economics editor of The Financial Times. He is one of the wisest observers of economic affairs that I know. And, notably, every article he writes is accompanied by, and is based on, four or five charts of historical economic and financial data—actual facts.

Regarding the advantage of doing the math, Ralph Waldo Emerson said it best: “Numbers serve to discipline rhetoric. Without them it’s too easy to follow flights of fancy.”

Learn From History

More than anything else, you must have a good understanding of economic and investment history because, in the words of Mark Twain, “History does not repeat itself, but it does rhyme.” Patterns that occurred in the past inevitably do recur in the same general way—again and again over many decades. Financial bubbles of stock market exuberance are an example.

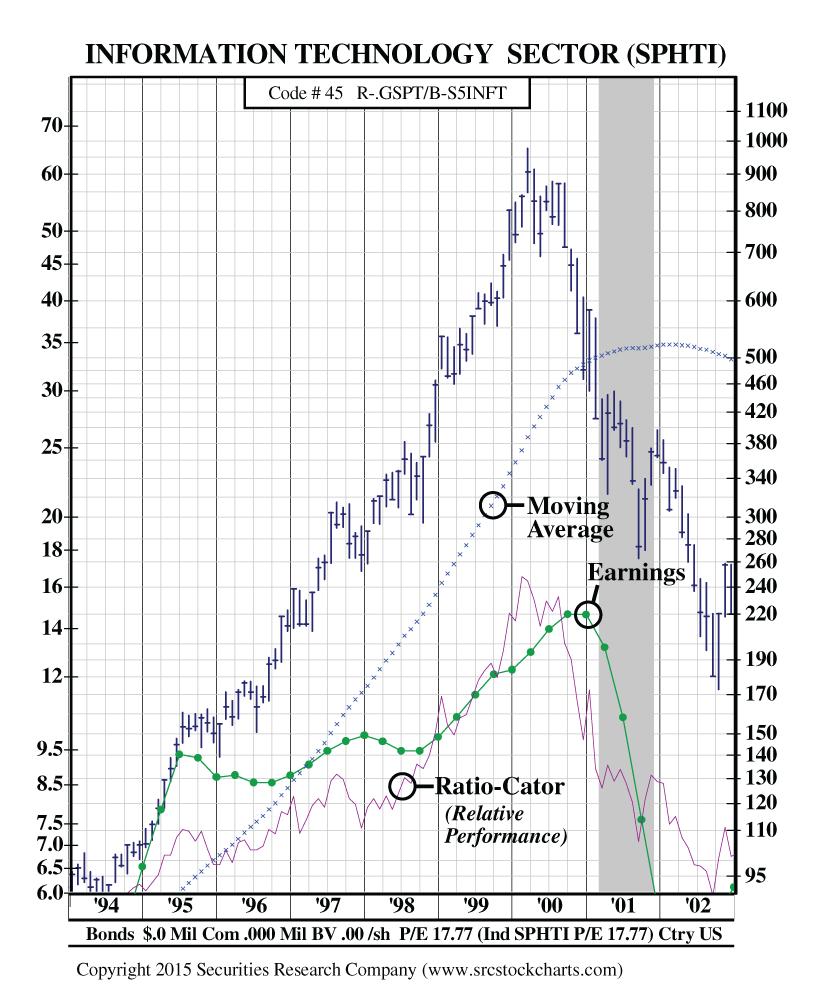

Thus, in 1999, it was clearly evident to experienced observers that legitimate investor enthusiasm for burgeoning new technology companies had escalated to the level of dangerous irrationality—and that a true bubble was forming in the stock market, with technology stock valuations reaching insane extremes. But that bubble continued for another year, sucking in more investors’ money, until it finally burst in February 2000. This led to market losses of 80% to 100% (see Figure 1). A very good history lesson.

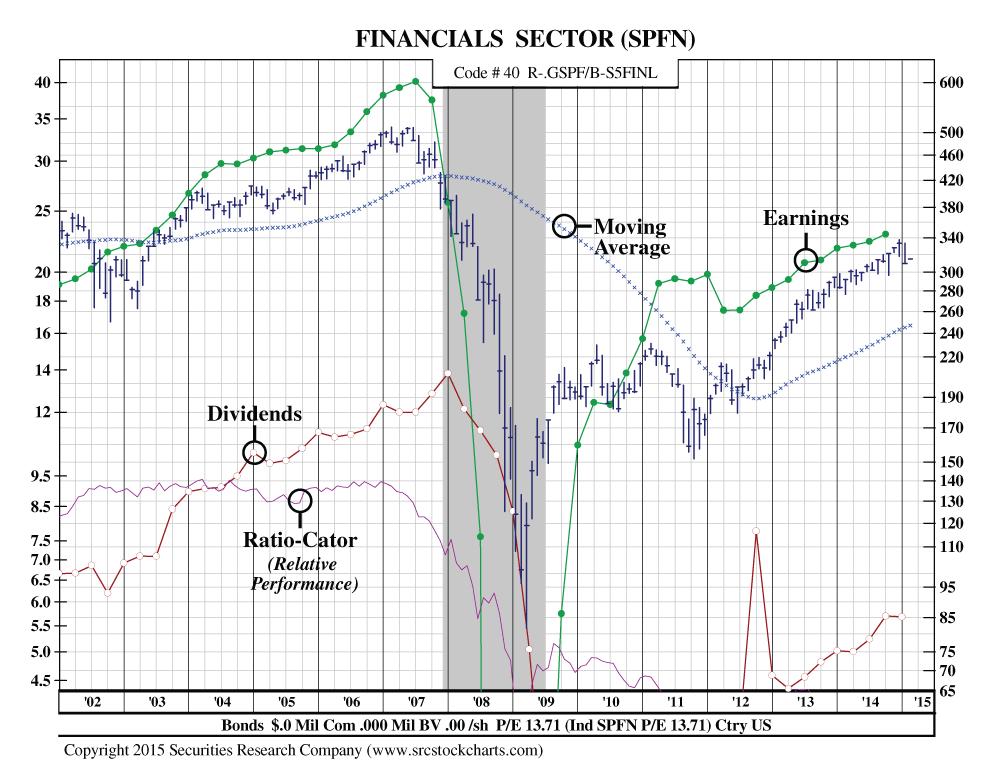

Similarly, in 2006 it became obvious to any thinking person that the unprecedented boom in home sales was being financed by loosey-goosey, extra-easy mortgage terms that were being scooped up by marginal and obviously incapable buyers, who had nowhere near the financial resources to ever pay such loans off. Inevitably, within a year the first cracks appeared, soon followed by massive loan defaults and a total financial collapse, as shown in Figure 2. But in the enthusiasm of the moment, very few lenders, regulators or investors recognized or faced up to the extreme excesses that had developed.

Remarkably, the patterns of these events matched exactly those of earlier bubbles, like in my lifetime the “Go-Go Market” in small unproven companies in exciting new fields in 1968 (which led to 75% price declines in 1969), and in oil stocks in the early 1980s when oil prices were pushed way up by several unusual events in the Middle East. (This caused oil stocks to double in a year, before falling back 45%—in historical terms just a modest bubble, but a big loser for all the investors who bought near the top.)

However, investors in later years had forgotten those bubbles or they had never heard about them. No wonder Emerson said, “The years teach much which the days never know.

Don’t Try to Be Smart, Just Use Plain Common Sense

We should be realistic, and really humble, about what we do know and about our abilities to make good decisions. And we should simplify our thinking as we observe the investment world, concentrating on fundamental, basic facts. This will also give us realistic expectations as to the returns we can earn for our portfolios. Optimism is a useful attribute for investors, but it must be tempered by common sense and grounded in facts.

Among other things, this means focusing on the quality of companies and the valuation of their shares.

Good quality derives from strong companies in favorably situated businesses. We’ve seen how General Motors (GM), the powerful leader in an unattractive business for many decades, has been a terrible investment for a long time, while Johnson & Johnson (JNJ), the strong leader in an excellent business, has been a highly rewarding investment. So find the leaders in fields where good growth and profitability give you a favorable tailwind, and go with the companies there that have the strongest competitive positions and the most solid finances. Such companies won’t enable you to get rich quickly, but they are the best means of earning above-average returns while taking below-average risks.

Pay Close Attention to Stock Valuations

This is critical to good investment performance. Valuation analysis shows us where the best and worst values are. Even an excellent company can be a terrible investment if its shares are overpriced. And the most rewarding purchases are always the shares of good companies that are temporarily undervalued by the market for some transitory reason. Essentially valuation is the discipline that screens out the emotional swings that derail many investors.

To counter such emotions and all the day-to-day focus on short-term “news” in the hurly-burly stock market environment, it’s very desirable to think always in a long-term context. This means basing our decisions on key fundamental factors about companies (not their latest quarterly earnings) and about industries. It also means using investment techniques that have proven successful over a long time. Again, this requires discipline.

Going along with that, one final attribute that investors need is patience. If you have a logical plan, always execute it at a favorable time, and wait for that time—thereby purchasing a stock you want to own only when its valuation is reasonable. It also means hanging onto a good stock when it’s in the doghouse with most investors for what is usually just a temporary snag in the business. (At such times, of course, the stock’s price is depressed so it would be an exceptionally imprudent sale.)

The most egregious and costly example of impatience I can recall is worth recounting here. In January 2000, a bright, younger friend called me and said, “Brad, I’ve finally decided this technology stuff is for real, so I’ve just put 25% of my 401(k) into two technology mutual funds.” Ouch!! He did this, in his ill-timed words, so as “not to miss the boat,” just six weeks before the peak of the tech bubble. And when the subsequent crash ended in 2002, his 401(k) had lost 20% of its total value. It has never recovered from that blow and now he’s forced to work all the way up to age 70, just to get a minimally adequate retirement income. Remember the old German adage: “We grow too soon old and too late smart.”

Investing is a fascinating activity and it can be very enjoyable (most of the time), if you do it as I have described here. So try to get that enjoyment out of it, as well as its financial rewards. I have, and I’m grateful for that.

Tags: David L. Babson & Co., doing the math, economic history, H. Bradlee Perry, investing experience, investment history, investment manager, investment process, make good decisions, managing investments, stock market, stock valuations