Oxstones Investment Club™

Oxstones Investment Club™Introduction

Michael C Jensen in his study entitled “The Performance of Mutual Funds In the Period 1945-1964” concluded his study with these words:

The evidence on mutual fund performance discussed above indicates not only that these 115 mutual funds were on average not able to predict security prices well enough to outperform a buy-the-market-and-hold policy, but also that there is very little evidence that any individual fund was able to do significantly better than that which we expected from mere random chance.

But the study was conducted many years ago. Has time proved him wrong?

Apparently not — if the Mid-year 2012 S&P Indices versus Active Funds Scorecard (SPIVA) is to be believed. The results show that indexes beat actively managed funds in almost every asset class, style, and fund category– the only exception being international equity where active outperformed the index that S&P selected.

Such studies and results have paved the way for an onslaught in the marketing and advertising of index funds where passive investing is lauded over active investing.

Active asset management is based on a belief that a specific style of management or analysis can produce returns that beat the market. The active approach seeks to take advantage of inefficiencies in the market.

Passive asset management, on the other hand, is based on the belief that markets are efficient and that market returns cannot be surpassed regularly over time.

However, all is not black-and-white in the world of investments. The fact that mutual fund results are not as good as indices does not imply that passive is altogether and all-the-time better than active.

In this entertaining article published by the New York Times, Warren Buffett is said to have told students at Columbia University that he had only one or two truly great investment ideas every year. “But the average mutual fund had 80 great ideas for you to buy today” — the article went on to say.

Perhaps, mutual funds in their efforts to increase sales, focus too much on product differentiation, promotion and marketing rather than on investment strategy?

Passively Active

Sprouting up in the midst of the battle between index funds and mutual funds are hybrids that capitalize on the combined relative strengths of passive and active strategies.

Some companies have incorporated risk factors such as value stock exposure, small cap exposure and even price momentum to arrive at what is sometimes termed as “super-beta” or “smart-beta” in order to re-weight an otherwise passive cap-weighted index.

Passive strategies earn better returns, on average, by default — they supposedly have reduced volatility and drawdown (not to mention lower fees). Manage volatility and the returns take care of themselves, so to speak.

But passive returns are market returns. And investors or managers sometimes turn to active strategies in the hope of getting a better return than the market. The problem is whether this extra return can be obtained without incurring too much extra volatility.

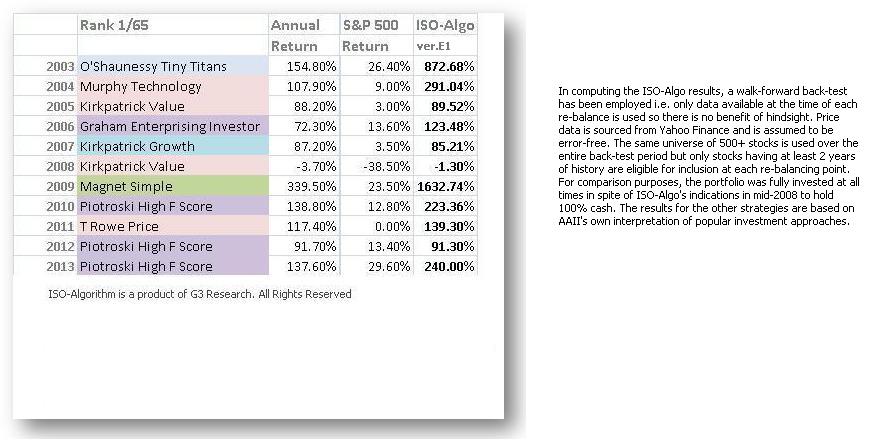

Let’s take a look at the simulated results of popular active strategies compiled by the American Association of Individual Investors. The figure below shows the top strategy in each year from amongst 65 different strategies plus the ISO-Algorithm.

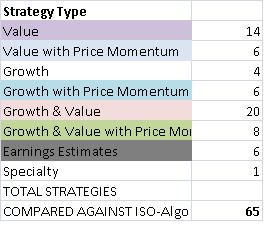

The 65 strategies are color coded as follows.

The top strategies in each year beat the S&P500 hands down. Closer examination reveals, however, that none of the top AAII strategies beat the other AAII strategies consistently. They also did not beat the S&P500 in every year.

See the figure below where the white cells are returns below the S&P500 return and the blue cells are returns above the S&P500. For comparison purposes, the strategies illustrated span the different strategy types.

ISO-Algorithm

The comparison above is not intended to be a rigorous determination of the best investment approach but the results of the ISO-Algorithm certainly warrant a further look at.

This strategy trades every 9 days so it is not for the investor who wants to take a passive approach. 9 days was chosen as the shortest possible horizon to test the outcome of a very active approach while still making formulaic sense.

The ISO-Algorithm is a quantitative strategy and not based on intrinsic value, news, technical indicators or economic forecasts etc. Instead, the strategy is based on price stochastics and attempts to profit from “noise” which in itself could be the result of actions based on intrinsic value, news, technical indicators or economic forecasts. More on this in a later article.

Interestingly, it is the only strategy that is consistently higher or nearly as high as the top-ranked AAII strategy in each year.

It is also the only strategy that never falls below the market return.

In the next couple of articles, I will be sharing with you some aspects of the ISO-Algorithm that make it different from most other strategies. I will also share a couple of formulas that you can readily incorporate into your own strategy, even if it is not a purely quantitative one.

Tags: active approach seeks to take advantage of inefficiencies in the market, Active asset management, active international equity outperformed the international equity index, active investing, active investing vs passive investing, active strategies. passive strategies, American Association of Individual Investors, efficient market theory, hybrid mutual funds, hybrids funds capitalize on the combined relative strengths of passive and active strategies, incorporating risk factors, index funds vs active funds, indexes beat actively managed funds in almost every category except international equity, investing lessons, investment research studies, investment strategy based on price stochastics, investment wisdom, ISO-Algorithm, Michael C Jensen, Mid-year 2012 S&P Indices versus Active Funds Scorecard (SPIVA), mutual fund performance studies, Passive asset management, passive investing, quantitative strategy, re-weight a cap weighted index, simulated performance results of popular active strategies, small cap stock exposure, smart beta, super beta, The Performance of Mutual Funds In the Period 1945-1964, the top investing strategy that consistently beat the S&P 500 index, the top ranked AAII strategy, top AAII strategies, value stock exposure, Warren Buffett, warren buffett quotes