Oxstones Investment Club™

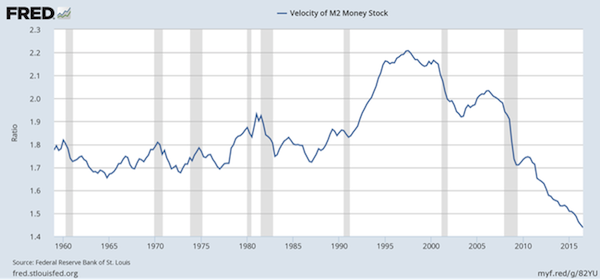

Oxstones Investment Club™Money velocity has been going down steadily for almost 20 years. After the great recession, it has dropped to a historically low level.

Quantitative easing and drops in interest rates never offset deflationary forces around the world. QE money went from the central banks to financial institutions, but did not enter the real economy.

Today, over $50 trillion in cash is there waiting to be used.

People are hoping for a reboot

The world economies have a lot of debt and might slow down at best. But there is hope that tax and regulatory reforms in the US could make more investments and help our economy.

Trump’s win led to a rally in the stock market. This trend may be premature. The rally now could be about hope, not real changes. Yet, there are good reasons to have some hope.

A few of Trump’s said goals are good for the economy. Lower corporate taxes without widening deficits could cause new investments in the US economy.

Add to this a strong effort to repeal heavy regulations and the business climate in the US could fast become preferred. The US should get multinationals to repatriate cash from abroad. Foreign companies should invest in productive assets here.

Then our economy would improve.

Why does it matter?

As cash gets spent, we may see a return to a historical level of velocity of money. Why does it matter? Central bank intervention post-2009 failed because money put into the financial system did not find the broad economy.

If corporations spend money on productive investment, they will make jobs. That, in turn, will cause higher consumer spending and more velocity. Higher velocity will mean more money will be chasing for goods and services. We may get the inflation the Fed has tried so hard to get over the past 10 years.

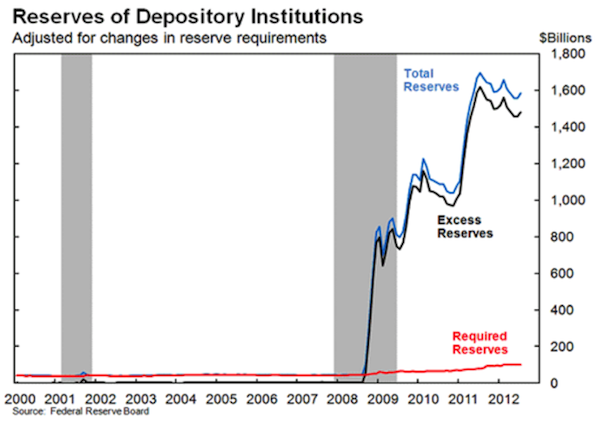

The banking system is laden with excess reserves sitting on the Fed’s balance sheet. If these reserves find the real economy, we will see a fast change. When the Fed realizes that inflation is back, it is likely to have taken hold. The Fed can raise interest rates fast.

But here’s a catch.

Americans can’t afford higher interest rates

The Fed holds nearly $20 trillion in debt.

They can’t afford higher interest costs. Nor can its heavily indebted citizens: American households have $14.6 trillion in mortgage, student, auto, and credit card debt.

Add to that another $13.4 trillion in US business debt, and the problem of rising interest rates becomes clear.

A more likely scenario is a more gradual pace of rate hikes by the Fed, even if inflation runs hot. In that case, we will see negative real interest rates for some time.

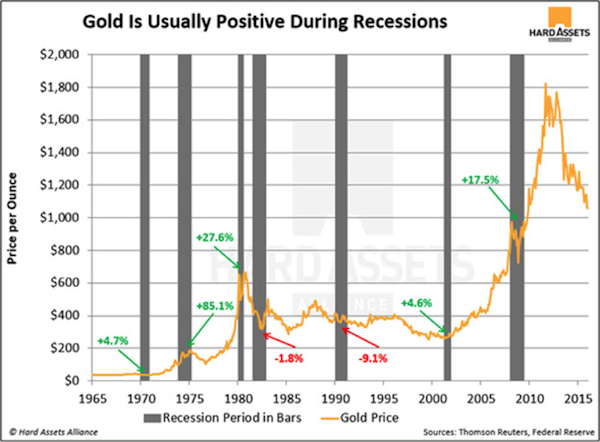

This is just the setting for investors to hold gold (see the chart below).

Not only as insurance against the risk of financial collapse, but also as a tangible investment that will appreciate.

What if Trump fails?

What if the Trump administration fails to turn around the economy? The headwinds created by a strong dollar and by increasing deficits could push the US economy into a recession that becomes global.

Then export dependent Germany, China, and Japan quickly enter a deep recession. The global financial markets are plagued by a banking crisis. The world central banks resume various programs of QE infinity and negative interest rates. They continue to de-base their fiat currencies.

The good news for gold investors is that even if the Trump administration fails, gold has historically been a reliable source of insurance against a recession.

In five of the past seven recessions, the gold price rose. And three of those times its soared double digits. In only one recession did gold suffer a noticeable decline, (-9.1% in 1990). Even in the midst of the 2008–2009 financial crisis, gold moved higher.

That why it’s another reason why investors should always have an allocation to gold as insurance.

Gold wins either way

Like many investors, I am hopeful the incoming administration can return the US economy to a sustainable path of strong economic growth. But hope isn’t a good investment strategy. That’s why I own gold.

If in the best case scenario, Trump successfully reverses the downward spiral in the velocity of money—creating inflation in the process—gold should shine. If not and the worse case scenario materializes with a fall back into recession (or worse), gold should benefit as well.

Either way, there is a compelling case to be made that every investor should own gold as an insurance policy.

Free Ebook: Investing in Precious Metals 101: How to buy and store physical gold and silver

Download Investing in Precious Metals 101 for everything you need to know before buying gold and silver. Learn how to make asset correlation work for you, how to buy metal (plus how much you need), and which type of gold makes for the safest investment. You’ll also get tips for finding a dealer you can trust and discover what professional storage offers that the banking system can’t. It’s the definitive guide for investors new to the precious metals market. Get it now.

Tags: corporate taxes, debt, deflationary forces, economic growth, financial collapse, great recession, interest rates, money velocity, productive investment, recession, regulatory reforms, stock market, Trump administration, US business debt, us economy