Oxstones Investment Club™

Oxstones Investment Club™It is a fundamental principle of portfolio management theory to include alternative assets as part of a well-diversified portfolio. One of the most popular alternative investments for savvy investors is real estate. For those looking to hedge their holdings against inflation and enjoy the potential of a steady cash flow stream, there are two primary methods to gain exposure to this relatively stable asset class: real estate investment trusts (REITS) and private equity real estate (PERE) funds. We look at the nature and history of PERE funds, their benefits and how they stack up against the REITs. (For more, see: How To Invest In Private Equity Real Estate & Can Real Estate Stabilize Your Portfolio?)

What Exactly is a Private Equity Real Estate Fund?

According to research by the Zell/Lurie Real Estate Center at the Wharton School of Business, sensing a need to amass a “war-chest” of equity to acquire delinquent foreclosed properties, the first pooled PERE fund was created by business magnate Sam Zell in the 1980s. While this pioneering firm raised a total of $409 million in capital, according to Preqin Research, the PERE sector has since grown to $742 billion in global assets under management as of 2014.

This large growth in popularity translates to millions of dollars in management fees, as PERE firms are actively managed, and much like hedge funds, the fund managers (or general partners) earn a percentage fee based on the total committed capital. Managers of PEREs also tend to invest along with the investors (limited partners or LPs), usually with a 3-10 percent capital contribution of their own, and are precluded from forming additional funds until the capital committed to the current firm has been substantially deployed.

Investors of PERE firms are generally institutional (pension funds, endowment funds, fund-of-funds, etc.) or high-net-worth individuals. These investors pool their contributions in closed-end “blind pools” in order to be deployed at the discretion of the general partner in a variety of real estate related investments, ranging in risk and returns and typically lasting three-to-eight years. The potential investments strategies that a PERE firm can pursue are:

- Core strategies that pursue well-diversified, low-risk/return, traditional asset classes (office space, retail, industrial and multi-family units) in established locations. Core strategies employ little to no debt, and seek to provide a steady stream of cash flows for the LPs.

- Core-Plus strategies employ a moderate amount of leverage, and tend to be more moderate in risk as well as return. Core-plus assets may be located in less established locations, and may require some form of value-additions.

- Value-Add strategies offer moderate-to-high risk and returns, and feature higher leverage than core or core-plus. The value-add strategy seeks to add value through the operation, re-leasing or re-development of acquired assets.

- Opportunistic strategies are high-risk, high-return strategies that target poorly-managed, vacant or obsolete assets. These strategies employ very high leverage and may involve acquisitions of entire companies or portfolios of assets, or require full development or conversion projects.

- Mezzanine Lending/ Distressed Debt are strategies employed by firms that are comfortable with owning the underlying assets in the event of borrower default, as the loans issued by the firms involved in this strategy have more aggressive terms than traditional lenders.

- Fund-of-Funds are funds that investment in third-party managed PERE firms, and offer a diversified investment solution for smaller investors seeking access to larger, exclusive firms.

Benefits Investing in PEREs

As previously mentioned, PERE funds are generally available only to institutional investors and high-net-worth individuals. However, members of the general public can gain exposure to PEREs through publicly traded private equity funds offered through firms such as The Blackstone Group LP (BX), Apollo Global Management LLC (APO) and the Carlyle Group LP (CG). Owing to their actively-managed nature, PERE funds present opportunities for savvy management teams to seek out and turn-around underperforming properties and create investor wealth by executing value-added initiatives. Furthermore, the private nature of PERE funds grant management teams more direct input in the course of daily affairs, without having to worry about the ebb and flow that is inherent in public equity markets. Moreover, this private nature affords management the flexibility to pursue a variety of strategies such as, subdividing or combining different properties and selling, financing or leasing the existing real estate portfolio by any number of criteria (geography, type, etc.)

PEREs vs. REITs

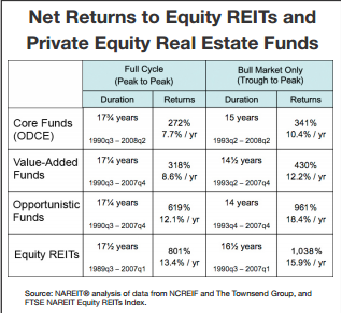

The performances of PEREs are often compared to their publicly traded counterparts: the REITs. Some investors are willing to give up the potential sources of alpha that come with the PERE’s active management, in lieu the REIT’s transparency, liquidity and accountability on the public market. A 2010 study by the National Association of Real Estate Investment Trusts (NAREIT) compared 17.5 years of data from the U.S. REIT market and private equity real estate funds, and found that public REITs outperformed core, value-added and opportunistic funds during the full market cycle. However, the study also found that during bull market stages of the cycle (trough to peak), opportunistic funds tend to outperform REITS on an annualized basis, owing to a shorter trough-to-peak period (although core and value-added funds continued to lag).

Figure 1 below showcases the net returns of PERE funds vs. REITs over the 1989/1990 to 2007/2008 span.

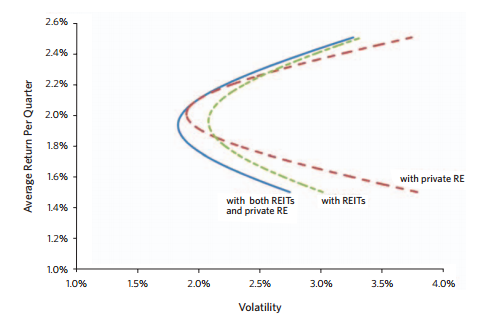

Furthermore, contrary to the notion that REITs experienced greater returns and higher short term volatility, a 2009 article by Investments and Pensions Europe, found that once PERE returns were “smoothed out” and appraised on a daily basis like stocks, the correlation between private real estate and REITs were found to be significantly higher and increased over time. The solution? Include both asset classes to create a better efficient frontier across all points on a risk-return spectrum (Exhibit B).

Exhibit B highlights the increase in risk-adjusted returns once REITs and PEREs are both added to a portfolio. (For more, see: How to Diversify with REITs.)

Source: BNY Mellon Asset Management

The Bottom Line

For investors looking to diversify into real estate, private equity real estate funds are a good way to gain exposure to this asset class. Although not as liquid or as transparent as REITS, PERE funds helmed by an experienced and proven management team, guided by a disciplined and focused investment strategy without an over reliance on leverage, can provide a high degree of risk-adjusted returns.

Tags: alternative assets, apollo global management, Blackstone Group, Carlyle Group, diversified portfolio, endowment funds, fund of funds, High Net Worth Individuals, high risk, high-return, investment strategy, management fees, pension funds, PERE funds, portfolio management, portfolios of assets, private equity real estate, real estate, REITS, sam zell