Oxstones Investment Club™

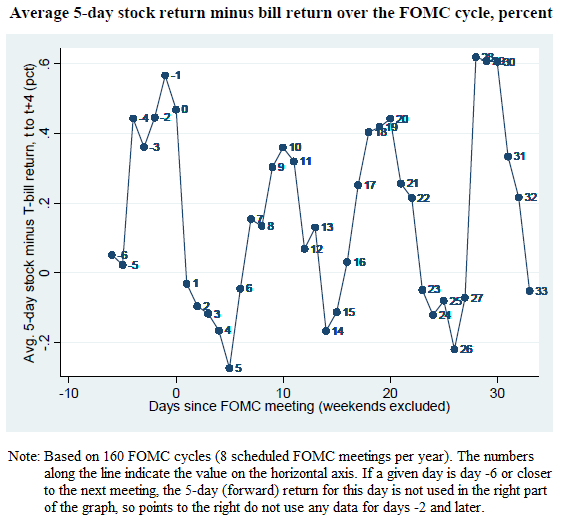

Oxstones Investment Club™David Blitzer, Chairman of the Index Committee for S&P Dow Jones Indices, recently highlighted research results showing excess returns are generated around FOMC meeting dates. The research paper, Stock Returns Over The FOMC Cycle, evaluates the average 5-day return minus the treasury bill rate. The paper shows statistically significant excess returns are generated in the five day period in advance of the FOMC announcement.

|

| From The Blog of HORAN Capital Advisors |

The paper notes the FOMC meeting dates are “quite irregular” and “‘even’ weeks in FOMC cycle time do not line up with other macro releases that would be influencing returns.”

Lastly, the paper looks at the unintended (and intended) information release that comes from the Fed. The report notes, “Overall, it is possible that the bi-weekly patterns in average excess stock returns and fed funds futures volatility result from both subtle intentional and unintentional communication coming from the Fed. The precise mechanism remains a central issue for understanding the economics behind our newly documented asset return patterns and an avenue that we (and hopefully others) will explore.”

As S&P’s David Blitzer notes in his article title, investors look for short term trading excess stock returns gains might consider to “Sell Just Before, Not After, the FOMC Meets.”

http://disciplinedinvesting.blogspot.com/2014/08/achieving-excess-returns-around-fomc.html

Tags: David Blitzer, excess stock returns, FOMC announcement, FOMC Cycle, FOMC meetings, influencing returns, investing tips, S&P Dow Jones Indices, short term trading, The Fed