Oxstones Investment Club™

Oxstones Investment Club™By Blake Ellis

At Finovate two dozen companies vied to be the next big thing in personal finance. From pay-by-smartphone to smarter banking, here’s what was new and cool.

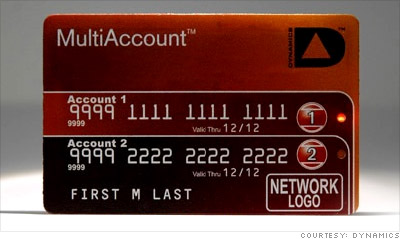

Imagine getting the bill at a business dinner and simply pressing a button on your personal credit card to transform it into your corporate card. Or checking out at a grocery store and pressing the same button to turn your debit card into your credit card.

Dynamics lets customers carry a single card but choose between multiple accounts when paying for items. Pressing a small button automatically reprograms the paper-thin card’s magnetic stripe — which is then swiped in a retailer’s credit card machine.

Other Dynamics cards let consumers choose if they want to purchase items using their rewards points or rewards cash. Worried about security? Another card variation hides account numbers until you punch in your personalized passcode — on the card.

Dynamics’ technology is creeping toward release: Citi has been testing the cards out with a limited group of customers over the last year, and Dynamics executives say they expect to soon be ready to announce other partnerships.

Burning to invest some money but don’t know where to start?

Launched in May, Betterment‘s investment service lets beginners — or sophisticated investors who don’t want to deal with portfolio rebalancing — blend stocks and bonds in one easy-to-manage account.

There’s no minimum balance requirement, and just one investing choice to make: What percentage of your money do you want in stocks? Betterment parks your cash in market-tracking index funds.

Do you ever look at your bank statement and wonder what keeps draining your balance each month?

Starting this month, BillShrink will show you just how much that AT&T cell phone plan or Time Warner cable service is hurting your bottom line, by tallying the amount you could be saving using alternative plans and allowing you to sign up immediately.

Addicted to your morning caffeine boost from Starbucks? BillShrink will even pinpoint a cheaper cup of joe in your neighborhood.

Link BillShrink to your bank account and its suggested savings will show up under related transactions that already appear on your bank statement each month.

There’s an added bonus: If your bank statement shows that you bought a sweater from Target or any other retailer BillShrink works with, that company has the option to offer you coupons for future purchases.

True to its name, Bundle pulls accounts from your various financial institutions and bundles them together in one place, showing you exactly how much money you are saving and spending.

The site displays the information in animated bubbles, and compares your spending habits with others from your community and demographic. You can see how much you spend on fancy dinners out compared to your neighbors — and how much more you’re paying for groceries than the average person in your same income bracket.

Bundle can then propose a more cost-effective budget for you, and show you cheaper alternatives to your current expenses.

One standout feature: Unlike other budgeting tools, Bundle lets you adjust on the fly. If you realize halfway through the month that you’re not going to spend all the money you budgeted for clothes but you need a little extra money for groceries, you can reallocate that money to another category without having to do the calculations in your head.

Launched in September, Bundle is already reeling in around 300,000 visitors per month.

As consumers spend more and more time with their smartphones, they’re increasingly looking to use them as their wallet, relying on apps to pay bills, transfer money and check account balances.

MFoundry builds those apps, selling a white-label system used by more than 200 banks and credit unions supporting more than 1 million users.

The system has some advanced features, allowing users to text their bank to find out their account balances and pay bills through an easy-to-navigate mobile interface.

Plus, you don’t have to trek to the bank when you need to deposit a check. Simply take a photo of the check and voila, it instantly shows up in your account.

MFoundry customers include Bank of America, Citi and PNC Bank. Though the company has been around for a number of years, its mobile services debuted in August 2010.

Instead of navigating through your bank’s website or fighting through the hold queue to connect to a representative by phone, ActivePath lets you execute bank transactions through e-mail.

Beginning this year, banks can use ActivePath’s system to e-mail their customers secure statements, deposit notifications and insufficient funds alerts. Customers can then tell the bank what kind of action they want to take — whether it’s make a payment, transfer money or get a loan.

ActivePath says the largest banks in Israel already use its service, and it is currently working with several large banks in the U.S. and Europe. But the banks prefer not to reveal their names for competitive reasons, ActivePath says.

Plantly is a matchmaker for investors, aiming to help all levels of investors find plans that best fit their risk tolerance.

You tell Plantly how much you want to invest and how long you want to invest it for, and the site will suggest diversified investment plans just for you — as long as you have at least $5,000 to throw in the pot.

Plantly shows you the amount of risk you assume with different plans, projects the returns you are likely to see, and customizes investment plans based on the fee structure of the broker you choose to work with.

No need for credit cards or cash — just swipe your phone at the register. Then broadcast your purchase on Facebook or Twitter to update your friends on what you just bought (if you want).

Sound weird? Yup — but not too weird for the 100,000 customers already using Blaze’s Mobile Wallet an average of nine times a day.

The service, which launched in September, lets card issuers give you a branded “sticker” to place on the back of any cell phone, which you can then use to make purchases. MasterCard is on board, and retailers including Best Buy, Rite Aid, McDonald’s and 7-Eleven have signed on to let customers make purchases with their Blaze stickers. These retailers can then offer rewards and coupons to customers at the point of sale.

Purchases are tallied in a mobile account — and it only takes a second to push a button and tell the rest of the world about the plasma TV you just “blazed,” if you opt to publish it via Facebook or Twitter.

It’s a wacky concept that’s a lightening rod for skepticism, but when a company like Blippy can raise $12 million in venture capital for a service that tweets out your credit card purchases, it seems like there’s room for even the craziest ideas to take off.

You probably haven’t heard of Yodlee, but you’ve almost certainly used it.

Yodlee knows who you owe money, what stock you just added to your portfolio and where you buy groceries.

The company is a financial data aggregation powerhouse, gathering information from more than 200 financial institutions and redistributing it to an array of portals and partner sites.

When you register at a site like Mint.com — a personal finance portal and one of Yodlee’s customers — you can choose to pull in information from dozens of different accounts, but Mint.com isn’t the one digging up that financial data. Yodlee is.

Yodlee has toiled quietly in the background for years. The company is now coming out of the shadows, packaging up its platform with a fancier user interface and creating a new app store it hopes partners will plug into.

The under-development Yodlee FinApp Store is drawing notice from some heavy hitters, including tax preparer H&R Block, which is working on an app.

Source: money.cnn.com

Tags: ActivePath, apps to pay bills, Betterment, BillShrink, Blaze Mobile, Blaze's Mobile Wallet, Bundle, cheaper alternatives, cool budgeting tools, cost-effective budget, deposit checks on your phone, Dynamics, execute bank transactions through e-mail, MFoundry, Multiaccount card, one easy-to-manage account, pay with cellphone, savings, Yodlee