Oxstones Investment Club™

Oxstones Investment Club™According to Freddie Mac, the average interest rate on a 30-year fixed rate mortgage rose by 8 basis points over the week to 4.39%. Since the beginning of the year, mortgage rates have risen by about 1 percentage point and are now at a level last seen in August 2011.

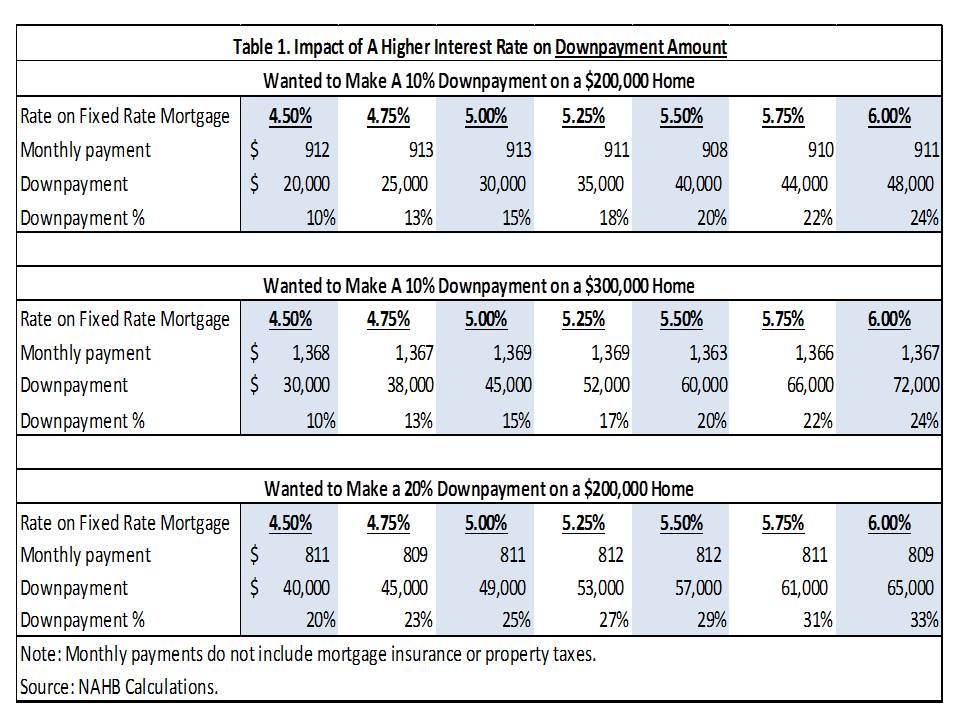

The rapid rise in mortgage interest rates could affect housing affordability through higher monthly mortgage payments. However, monthly mortgage payments are not the only path by which rising interest rates can affect affordability. Homebuyers can instead decide to raise their downpayment amount in order to maintain an otherwise constant monthly payment in the face of rising rates.

Table 1 shows the impact of rising mortgage rates on downpayments for this scenario. As interest rates rise, homebuyers increase their downpayment in order to keep monthly mortgage payments roughly the same. However, the required increase in the downpayment, both in levels and as a share of the house price, declines as mortgage rates rise. If the downpayment remained at 10% even as mortgages rates rose, then the monthly mortgage payments on a $180,000 mortgage, $912 at a 4.50% mortgage rate, would rise to $994 if mortgage rates rose to 5.25% and to $1,079 if mortgage rates rose to 6.0%.

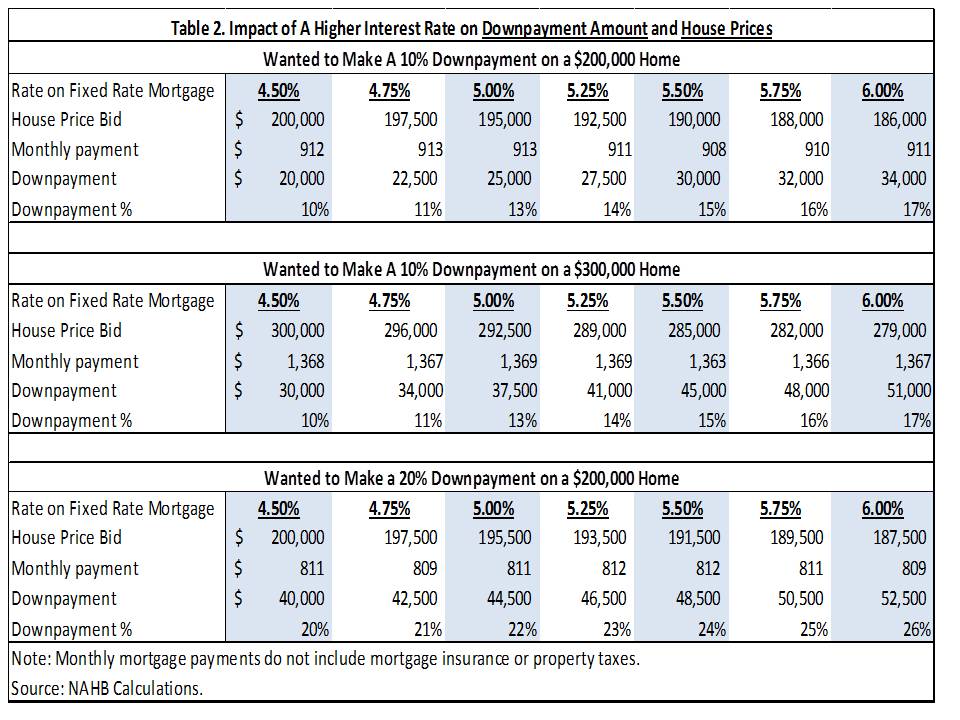

Alternately, homebuyers seeking to maintain affordable monthly mortgage payments may lower their bid price on a home. In aggregate, lower bids that are accepted by house sellers could depress house price growth, partly offsetting recent gains.

Table 2 assumes, as an example, that the total cost of higher mortgage rates is evenly split between a lower bid and a higher downpayment in order to maintain affordable monthly mortgage payments. the required downpayment percent rises as in Table 1 but at a slower rate.

This exercise illustrates that rising mortgage rates can increase monthly mortgage payments, but a larger downpayment can offset this effect. However, accumulating a larger downpayment may be difficult, especially for recent homeowners with little home equity, as well as first-time home buyers.

These numbers illustrate a large issue challenging the demand side of the housing market, which is connected to the issue of pent-up housing demand. Obtaining a mortgage to buy a home, including accumulating the necessary downpayment, is in many ways a greater hindrance for the market than recent rate increases.

Regardless, rising mortgage interest expense by homeowners is a reminder of the importance of the mortgage interest deduction (MID) in terms of supporting housing demand. As prospective homebuyers face larger interest payments, the value of the MID increases.

Tags: downpayment, fixed rate mortgage, Freddie Mac, homebuyers, housing affordability, mortgage payments, Mortgage rates