Oxstones Investment Club™

Oxstones Investment Club™Nomura, as part of an excellent report looking at various aspects of active versus passive investment management, have considered Warren Buffett’s famous bet that an index fund will beat a fund of hedge funds over ten years.

Buffett is winning, and the bank’s conclusion is that this is very far from a fluke:

In our view, alternative assets as a group show consistently poor performance. Beta is high. Alpha is near zero, if not negative. Correlation with standard asset classes is high. Return and diversification benefits are negligible.

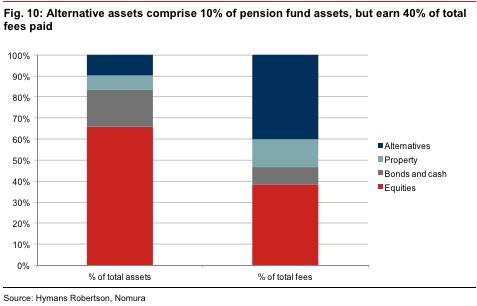

More on that below, but first note the proportion of pension fund fees going to the alternative investment fund managers. Never have so few been paid so much by so many for doing so little.

A chart for pension fund trustees to keep in one hand while they regard the breakdown of returns from their hedge fund and private equity managers in the other.

The [Hyman Robertson] study estimated that British public sector pension funds paid approximately GBP 300 million (about USD 500 million) per year in management fees to alternative asset managers. To put this in context, the pension funds paid about GBP 250 million per year in fees to equity managers, even though equities accounted for 65% of their portfolios.

Before we get onto the details of Nomura’s work, consider the steady progression of evidence that supports the bank’s conclusion, and who is saying it.

The academy was there first, in relative obscurity. This paper found that investment hedge fund skill does not exist over meaningfull timeframes — there is no persistence, so good investment performance does not signal more good investment performance in the future.

This paper found that investors in hedge funds received about the same investment return as holding Treasuries between 1980 and 2008, and much less than if they has just bought stocks.

This one, which found pension funds actually have shown some ability at stock selection, discovered that they are hopeless at picking alternative managers.

And this paper revisiting stylised facts about hedge funds found that most fail, with two-thirds of those funds reporting to databases now dead.

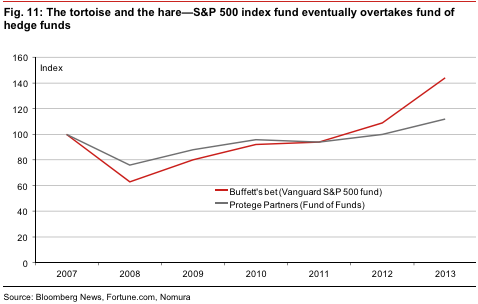

Warren Buffet made his 10 year bet with Protege Partners, an alternatives manager, at the start of 2008. Here’s how it’s doing so far:

Simon Lack, a former investor in hedge funds for JP Morgan, wrote the 2012 book on his experiences, The Hedge Fund Mirage. As well as a discussion of the many problems with trying to invest in hedge funds, the central claim was that all investment profits over and above the risk free rate (ie, owning US government debt) went to hedge fund managers as fees. He did choose one of the hedge fund indices with the worst performance to make that claim, but industry attempts to discredit his work largely served to vindicate his analysis.

Day to day, reporting spectacular bets that have paid off for individual hedge fund managers still makes for good stories about the hedge fund industry. But John Paulson did everyone a favour by being the genius of the financial crisis who made several fortunes betting agains mortgage backed securities only to then look like an idiot in 2011 when his flagship fund halved in value.

Meanwhile, in the years since 2008, it has become hard to miss the poor overall investment performance recorded by alternative investments, or that the names of top performing hedge funds tend to change from year to year.

Which brings us to Nomura. Some might expect banks not to explore the failure of alternatives too closely, given that actively trading hedge funds make for good customers and it is helpful for them to have plenty of capital to play with. But if clients are interested, the research departments will start to deliver.

The bank’s Anthony Morris and Tam Rajendran understand the reasons why investors are attracted to alternatives:

It comes as a surprise that the hare falls behind and ultimately loses to the tortoise in Aesop’s fable. In the same way, it comes as a surprise that a passive product outperforms an alternative product, which is supposed to convey the best of the best in active management talent.

But the reasons behind both surprises are related. Having the ability to outperform is not the same thing as actually delivering the outperformance.

They also list the reasons why a hedge fund manager might scoff at the idea that Protege Partners have “failed”, essentially the arguments typically made in favour of alternatives: investment “Alpha”, diversification, equity like-returns but with lower volatility, and access to non standard markets, managers, and sources of return.

Unfortunately:

Even by broader definitions of success, the Protege alternatives seem to have failed.

The authors start with some assumptions about alternative assets as a group, based on what they have found from previous work:

• High beta: Contrary to what the ‘alternatives’ label suggests, most fund benchmarks had high correlation to standard equity exposure and statistically significant, positive beta.

• Low alpha: Contrary to the positioning of alternative products as alpha providers, there was little evidence of manager skill. Alpha was statistically insignificant if not negative.

• Leverage management: Some alternative products, especially funds of hedge funds, seemed to target a volatility lower than equities. Other products, such as private equity, seemed to target a volatility that was higher than standard equities.

This left us with a basic model of alternative asset returns. To achieve the returns of hedge fund portfolios:

1) start with basic market exposure using the S&P 500 index or a rolling short VIX position,

2) reduce leverage to achieve an exposure of somewhere between 30% to 60% of standard, and

3) deduct fees.To achieve the returns of private equity:

1) start with a basic market exposure like the S&P 500, but more particularly the S&P Midcap 400,

2) increase leverage to achieve an exposure of somewhere between 120% to 150% of standard, and

3) deduct fees.

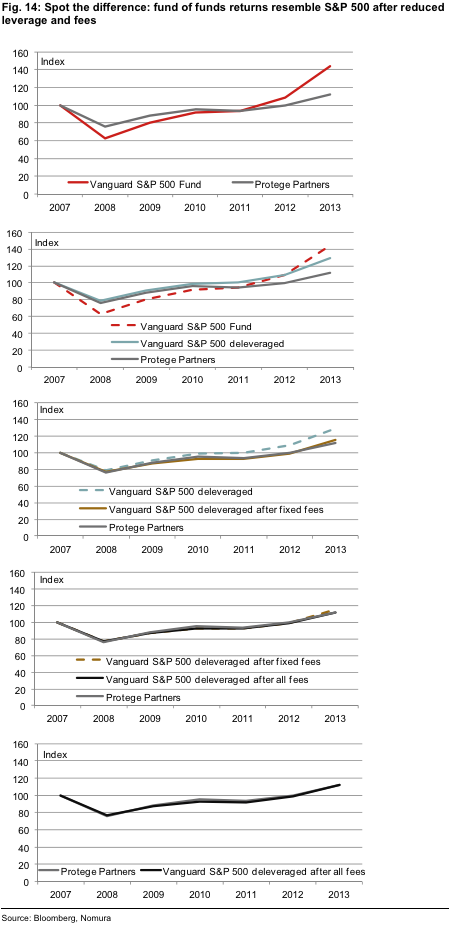

Which prompts a game of spot the difference.

Starting with the Vanguard S&P 500 fund, we de-leverage it (to achieve a 57% exposure, which is the beta of Protege Partners to the Vanguard S&P 500) and then deduct both fixed and performance fees. What we are left with is virtually indistinguishable from the performance of the Protege Partners fund of funds.

It turns out that this is not just Protege, however. The fund of funds industry has failed in a similar way, and investing directly in hedge funds to avoid the extra layer of fees doesn’t help either. Since 2008 hedge fund “alpha” has been negative while beta — the extent to which portfolio movements mirror the stock market — has increased.

Also, here’s Nomura’s demolition of that low volatility point, with our emphasis:

One of the advantages hedge funds are said to offer is lower volatility of returns. Looking at the betas, lower volatility of returns seems to be a product of reduced leverage, and not skill. While outperformance may be harder to achieve, volatility is easier to control. Reducing the leverage can deliver just that – low volatility of returns. But no-one should earn high fees for simply lowering volatility this way.

Those arguments about returns and diversification are hollow also:

Returns are similar to de-leveraged equities and diversification benefits are undermined by high correlations and significant beta to the market.

For private equity, which deserves its own series dedicated to measurement problems and fees, the authors come up against the familiar lack of data that a cynic might think is intentional given the claims for an illiquidity premium — higher returns for locking money up in investments for years at a time.

The lack of data makes substantiating such claims impossible, but Nomura finds returns very highly correlated with mid-cap stocks, just more leveraged.

They also find suspect the idea that everyone is above average (again, our emphasis):

To a large extent, private equity promoters are aware that there is some kind of performance problem in their industry. For this reason, marketing documents that we have seen describe the returns investors can achieve in private equity by referring to return data from the top quartile of private equity managers. This is done because the returns from a sample that included all private equity managers would not look impressive.

For the statistically-minded, this practice is a whopper. First, how can anyone claim to represent an investment opportunity by ignoring the lower 75% of the sample data? Second, there is an implicit presumption on the part of the promoter that they will be in the top 25% in the future. This practice is not only presumptuous, but also contrary to the results of a whole literature on the empirical analysis of fund manager returns.

Asset allocation funds are also found wanting. Which leads to the general conclusion that active management does not deliver. There is much work that has found money managers trying to beat a benchmark fail, in aggregate, the effect of fees is too great. Nomura finds that active managers not tied to benchmarks and free to invest as they see fit, fail also.

Any broad dataset is bound to have outliers. There might be true ‘alternatives’ out there, ones that offer real diversification and significant alpha. But, in our view, it is extremely hard to tell the good from the bad ex-ante. In any case, as the evidence shows, alternative managers as a group offer no alpha and very little diversification.Outperformers, even if they exist, are likely to be more the exception than the rule.

The tortoise don’t need big fees, the tortoise just keeps plodding. More in the usual place.

http://ftalphaville.ft.com/2014/08/01/1914342/the-hare-gets-rich-while-you-dont-back-the-passive-tortoise/

Tags: alternative asset managers, alternative assets, hedge funds, hedge-fund industry, investment performance, investment profits, leverage management:, passive investment management, pension funds, private equity managers, Protege Partners, Vanguard S&P 500 fund, Warren Buffett