Oxstones Investment Club™

Oxstones Investment Club™From http://seekingalpha.com/article/1107001-making-buffett-s-alpha-your-own

Much has been written about Warren Buffett’s investment acumen and philosophy. After all, the Oracle of Omaha’s personal wealth is now the value of all of the goods and services produced by the other 1.8 million people in his home state of Nebraska semi-annually. If you could go back thirty years, and buy one single stock or mutual fund, you would buy Berkshire Hathaway (BRK.A). What if I told you that understanding a few simple ideas could allow your investment portfolio to duplicate or even exceed Buffett’s performance over long time intervals?

Berkshire Hathaway now employs 275,000 people in its range of businesses. Built over the course of five decades, the conglomerate is the life’s work of one of the great investment minds of our time. Boiling down this extraordinary track record to only two simple ideas could have produced replicable returns – use of leverage and capturing the low volatility anomaly.

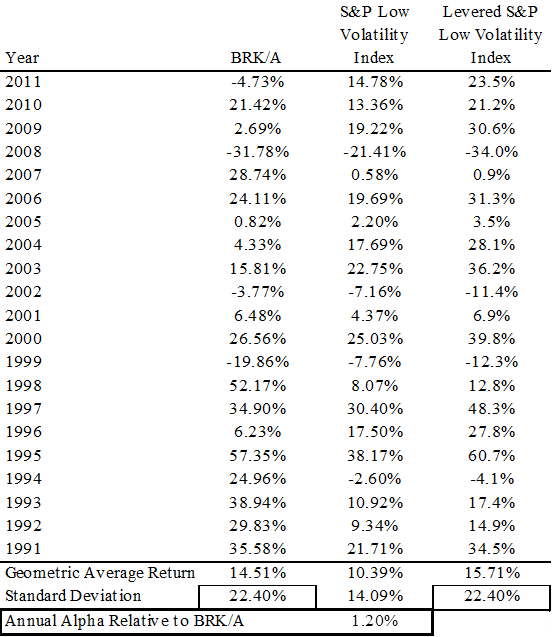

Below is a side-by-side comparison of Berkshire Hathaway’s stock, the returns of the S&P 500 Low Volatility Index, and the hypothetical returns of a version of the S&P Low Volatility Index levered to equate the volatility of its returns to that of the historically riskier Berkshire Hathaway. This low volatility index, replicated through the S&P Low Volatility ETF (SPLV), holds the one-hundred constituents of the benchmark S&P 500 with the lowest trailing realized volatility in inverse proportion to that volatility, rebalanced quarterly. Since the index’s advent in 1991, the levered low volatility index actually would have outperformed Berkshire Hathaway – the single best investment of the trailing generation.

(click to enlarge)

While Buffett may be the most written about investment professional of the last century, and is currently on the road pitching a new biography, few studies have been undertaken to ascertain how he has produced his extraordinary returns. Recently, Andrea Frazzini, David Kabiller, and Lasse Pedersen, each affiliated with hedge fund AQR Capital Management, published “Buffett’s Alpha,” which deconstructed the return profile of Berkshire Hathaway. From their analysis, “the general tendency of high-quality, safe, and cheap stocks to outperform can explain much of Buffett’s performance and controlling for these factors makes Buffett’s alpha statistically insignificant.”

The Low Volatility Anomaly

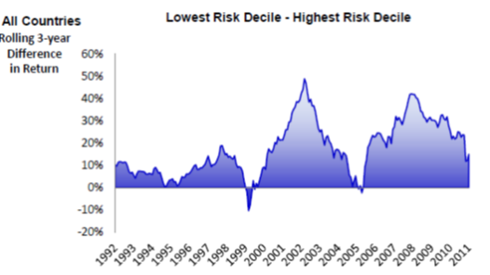

Since the groundwork behind the Modern Portfolio Theory was laid fifty years ago, it has been axiomatic that riskier portfolios should expect to be compensated with higher returns. More recent academic research has shown that this assumption holds less well at the extremes – the least risky stocks tend to outperform the most risky stocks on both a risk-adjusted and an absolute basis. In a 2012 paper by Nardin L. Baker of Guggenheim Investments and Robert A. Haugen of Haugen Custom Financial Systems entitled “Low Risk Stocks Outperform within All Observable Markets of the World,” the pair demonstrated that in their thirty-three country sample the highest risk decile of stocks, rebalanced monthly, underperformed the lowest risk decile of stocks in each locale.

(click to enlarge)

In the aforementioned paper by Frazzini, Kabiller, and Pedersen, the authors determined that the public stocks owned by Buffett in 13F filings had only a market beta of 0.77 from 1980-2011. Over that thirty-one year period, Buffett outperformed the market while owning in the public portion of his portfolio securities which on average had only three-quarters of the market beta. At the 1999 Berkshire Hathaway Annual Meeting, Buffett, during the rising crescendo of the tech bubble stated: “We’re more comfortable in that kind of (traditional) business. It means we miss a lot of very big winners. But we wouldn’t know how to pick them out anyway. It also means we have very few big losers – and that’s quite helpful over time. We’re perfectly willing to trade away a big payoff for a certain payoff.” From the chart above by Haugen and Baker, the end of the 1990s was the period when the most volatile stocks were actually outperforming the least volatile stocks as earnings multiples for start-ups in the tech space reached stratospheric heights. Buffett, as his 1999 quote illustrates, chose to pass and his relative performance in the short-run faltered, but over the long run he avoided the tech bubble-fueled market meltdown. Missing these major market corrections has been a predominant source of Buffett’s sustainable alpha.

Leverage

If owning low volatility stocks produces excess return per unit of risk, then levering these low volatility stocks allows investor’s with a higher risk tolerance to tailor their desired volatility and amplify their returns. In my earlier comparison of the levered Low Volatility Index and Berkshire Hathaway, the leverage that I solved for to equate the variability of returns was 1.59x. In “Buffett’s Alpha,” the authors found that Buffett “applies about 1.6-to-1 leverage.” It is hard to imagine this fact being merely a numeric coincidence. Berkshire has benefitted from the low cost of funds sourced through the float of his insurance subsidiaries as well as the fact that the firm’s publicly issued debt has enjoyed high ratings and low interest cost historically.

Of course, adding more than a half a turn of leverage is not as easy as running a calculation in an Excel spreadsheet. While institutional investors can seek financing from a prime broker in the form of margin financing, employing derivatives, or through a synthetic prime brokerage relationship, these strategies will still typically have the inherent risk of margin calls. Buffett’s use of insurance float does not carry this risk, and has historically been a cheaper source of funds. Buffett has also had the benefit of issuing term debt carrying a AAA rating, which Berkshire enjoyed from 1989-2009. Berkshire Hathaway, despite its recent nominal downgrades, can still issue thirty year debt at a spread of inside 100 basis points over Treasuries. Given the deductibility of corporate interest expense, this long tenor term debt has an after-tax cost of roughly 2.5%. If inflation averages 2.5% over that future time period, then Berkshire Hathaway can borrow at a real after-tax cost of zero.

Buffett certainly has a financing advantage, but the low interest rate environment has muted this benefit to some degree. Even an individual investor with unblemished credit can currently borrow for thirty years at 3.4%, secured by residential property. Like Buffett’s term debt, this debt is not subject to a call and currently benefits from the deduction on mortgage interest expense, reducing the after-tax cost of debt. If an investor has home equity, they can borrow against this equity for thirty years and use the proceeds to buy low volatility equities; bootstrapping together a levered low volatility portfolio that has historically had the same risk profile as Berkshire Hathaway. Both institutional and individual investors should think about ways to borrow non-callable long-term debt at today’s low borrowing costs – levering lower risk stocks instead of owning unlevered higher risk stocks has historically produced sustainable alpha.

Like much of the academic research emanating from Clifford Asness’ AQR Capital Management, “Buffett’s Alpha” is fantastic, and I encourage anyone with an interest in financial theory to read it. Given Buffett’s visible profile, the academic paper was chronicled in a wide range of well-regarded business periodicals. None of these pieces, or the remarkable original work by Frazzini, Kabiller, and Pedersen, boiled the important concepts into an easy to replicate trade. Hopefully, this is where my article offers value to Seeking Alpha readers. Owning the PowerShares S&P 500 Low Volatility ETF , levered up by 60%, has historically equated to the risk profile of Berkshire Hathaway, and well-grounded financial theory suggests that this strategy will perform as well or better prospectively.

Individual and professional investors alike can buy the stock of Berkshire Hathaway, run by an 82 year old chairman and CEO and in part by an 88 year old vice chairman, or use these tools to build their own investment powerhouse. Follow me to read coming articles about strategies for adding additional sources of premia not traditionally captured by Berkshire, and an additional strategy that does not employ leverage and has outperformed the S&P 500 (SPY) by 3% per year for the trailing twenty years.

Tags: BRK-A, BRK-B, capturing the low volatility anomaly, deconstructed the return profile of Berkshire Hathaway, levered low volatility index, low cost long tern debt financing, low volatile stocks, replicating warren buffett's returns, S&P 500 Low Volatility Index, splv, use of leverage, warren buffett berkshire hathaway