Oxstones Investment Club™

Oxstones Investment Club™Jared Kushner, Donald Trump’s son-in-law and top adviser, wakes up each morning to a growing problem that will not go away. His family’s real estate business, Kushner Cos., owes hundreds of millions of dollars on a 41-story office building on Fifth Avenue. It has failed to secure foreign investors, despite an extensive search, and its resources are more limited than generally understood. As a result, the company faces significant challenges.

Over the past two years, executives and family members have sought substantial overseas investment from previously undisclosed places: South Korea’s sovereign-wealth fund, France’s richest man, Israeli banks and insurance companies, and exploratory talks with a Saudi developer, according to former and current executives. These were in addition to previously reported attempts to raise money in China and Qatar.

The family, once one of the largest landlords on the East Coast, sold thousands of apartments to finance its purchase of the tower in 2007 and has borrowed extensively for other purchases. They are walking away from a Brooklyn hotel once considered central to their plans for an office hub. From other properties, they are extracting cash, including tens of millions in borrowed funds from the recently acquired former New York Times building. What’s more, their partner in the Fifth Avenue building, Vornado Realty Trust, headed by Steve Roth, has stood aside, allowing the Kushners to pursue financing on their own.

Kushner Cos. says it will prevail. Laurent Morali, the president, said the company has a variety of contingency plans for the building and its broader portfolio will allow it to sustain any setback. He said he is encouraged by the interest of several potential investors, but declined to name them.

“Reports that portray it as a distressed situation are just not accurate for the building or for the company,” Morali said in an interview on the 15th floor of the building, 666 Fifth Avenue.

But there are challenges all around. The mortgage on their tower is due in 18 months. This has led to concerns that Kushner could use—or has perhaps already used—his official position to prop up the family business despite having divested to close relatives his ownership in many projects to conform with government ethics requirements. Federal investigators are examining Kushner’s finances and business dealings, along with those of other Trump associates, as they probe possible collusion between the Kremlin and the Trump campaign. Kushner has already testified twice before closed congressional committees and denies mixing family business with his official role.

This article, which describes new details of the company’s troubled finances and its overseas fundraising efforts, is based on a review of thousands of pages of financial documents and interviews with more than two dozen executives, business partners, real estate agents, deal participants and analysts. They spoke on condition of anonymity to discuss private deals. Some feared legal reprisals or other retaliation from one of the country’s most powerful families.

The portrait that emerges is that of a real estate company established by a pair of penniless Holocaust survivors, its extraordinary expansion by their children, the rise of a grandson to a top White House role and a big bet that has complicated its financial future.

It was 2006—the height of the real-estate market boom—when Kushner Cos. agreed to buy 666 Fifth Avenue for $1.8 billion, then a record for a Manhattan building. All of it was borrowed except for $50 million. The company still holds half of a $1.2 billion mortgage, on which it hasn’t paid a cent. The full amount is due in February 2019.

The strain has become increasingly evident across their holdings. One person familiar with the company’s finances describes the tower, with its low ceilings and outdated floor plan, as the Jenga puzzle piece that could set the empire teetering.

The family’s idea of how to salvage its investment requires razing the building to the ground and constructing an 80-story tower with greatly expanded retail areas and high-end condominiums. No short- or medium-term return can be expected from such an aggressive approach. Even a return over the long run would be speculative, though Morali describes the plan as “ambitious and creative.” That narrows the pool of investors to those interested in something other than profit. Real estate experts say this almost certainly precludes U.S. companies. More likely: a foreign firm looking to get capital out of its country or seeking a trophy Manhattan property.

Before Trump began his rise to the presidency and the 36-year-old Kushner became his senior adviser, 666 Fifth Avenue struggled to attract serious offers. Meetings the Kushners requested were often rejected. After Trump’s nomination, billions of dollars in Asian and Middle Eastern money came under discussion. Two potential deals that made it to advanced stages, with China’sAnbang Insurance Group and a top Qatari sheikh, fell apart.

The new status meant the Kushners’ calls were more readily answered—but they came with additional scrutiny, not only of the Kushners but also of the investors. Since January, the company has ceased entering into business relationships with sovereign entities, Morali said. Federal investigators want to know if the Fifth Avenue building’s finances came up in a post-election meeting Kushner had with the head of Russia’s state-controlled development bank.

The Kushners have reason to look far afield. Even after selling big sections of 666 Fifth in 2011, they have increased their own vulnerability by borrowing more money for other deals, people close to the company say. After a refinancing, the deed to 666 Fifth sits in an escrow account, ready to be seized by lenders in a default, an action indicating their trust has grown thin. The mortgage will become even more of a burden after a scheduled jump in interest rates in December. Under some dire circumstances, guarantees in the refinancing agreement could even give lenders the ability to go after the family’s other assets—many of which are also underpinned by debt.

Towering Debt

While 666 Fifth Avenue has been a drain, Kushner Cos. has continued to make big moves across New York City, and company officials say those assets insulate the business. It has expanded its footprint by $1 billion, including the Times building and properties formerly owned by the Jehovah’s Witnesses, according to data firm Real Capital Analytics. Morali, sitting in a conference room below a painting of the company’s founders—Jared Kushner’s grandparents—says even a worst-case scenario at 666 Fifth would do minor damage to the company, because “it’s just one small piece of the portfolio.”

But after selling 18,000 mid-Atlantic apartments in 2007, the Kushners only partially own a substantial number of the company’s assets. In many cases, Kushner Cos. has partnered with well-capitalized firms that want to invest in real estate and seek out experienced locals for deals. These include the Israeli firm Gaia Investment Corp. as well as Oaktree Capital Management, the Los Angeles-based asset manager, and Stonehage Fleming, a London firm that invests money on behalf of 250 wealthy families primarily from Europe, the Middle East, and Africa.

As a privately held business, Kushners Cos. doesn’t generally have to disclose how ownership breaks down between it and its partners, and Morali declined to provide details. But there are clues. One Brooklyn development site purchased in 2014 for about $75 million and heralded by the real estate press as “Jared Kushner’s big Gowanus project”—so-named for the canal it abuts—is in fact barely owned by the Kushners at all. SL Green Realty Corp., their partner in the endeavor, owns 95 percent of it, according to a regulatory filing. The remaining 5 percent is split between the Kushners, and LIVWRK, another developer. Elsewhere in Brooklyn, where the Kushners partnered with RFR Realty to purchase buildings owned by the Jehovah’s Witnesses, they own about half of the project’s equity.

It’s here where the Kushners have scaled back. Among the six buildings the partnership purchased for $375 million in 2013 is a 30-story hotel at 90 Sands Street scheduled to be turned over to the Kushner group later this year. Kushner Cos. is now exiting the partnership and selling its stake to RFR, Morali said. Leaving the property means narrowing its role in a planned tech-centric Brooklyn office hub—its most ambitious project since purchasing 666 Fifth.

Kushner Cos. New York Area Properties

666 FIFTH AVE.

229 W 43RD ST.

1 JOURNAL SQUARE

TRUMP BAY STREET

55 PROSPECT ST.

117 ADAMS ST.

81 PROSPECT ST.

77 SANDS ST.

90 SANDS ST.

175 PEARL ST.

The Kushners are also extracting cash from properties in which they do own significant stakes. Six floors of the former New York Times building, which they purchased for $295 million in 2015, now have $370 million of debt against them, loan documents show. Of that amount, at least $59 million was used to return cash to the Kushners.

Across the Hudson River at Trump Bay Street, a luxury residential building in Jersey City, the family plans to take out $50 million, Bloomberg previously reported. Efforts over the summer to obtain a $250 million mortgage for the property struggled in the face of controversy around their use of an investment-for-visa program. Now the company has found a lender, Morali says, declining to name the firm.

Central to the fate of 666 Fifth yet noticeably absent from the gyrations around it, is Steve Roth, Vornado’s chairman and chief executive officer, whose firm owns almost half the building’s offices and most of its stores following a 2011 refinancing. When an analyst asked Roth about 666 Fifth in an August earnings call, he demurred, saying the issue was being debated. Two spokesmen for Roth declined to comment for this article.

In 2014, at a meeting in his 57th Street headquarters with Jared Kushner and his father, Charles Kushner, as well as others wrestling with how to save the investment, Roth argued against the Kushners’ extravagant renovation plans, saying, “It would be worth a lot more if it was just dirt,” according to two people who were there.

Roth is famous for his unsentimental patience. In an April letter to investors concerning a recent dip in demand for retail property, he described an opportunity to “feed on the carnage” for those with ample capital at their disposal—a chance to profit from the overleveraged and underprepared.

That’s what Roth saw when his firm came to Kushner’s rescue in 2011, according to three people familiar with his thinking at the time. For $80 million and the assumption of half the debt, Vornado put itself in the best position to become 666 Fifth’s sole owner in the event of a restructuring or worse.

This may help to explain why Vornado has allowed Kushner Cos. to shoulder the burden of hunting for potential partners and lenders, according to four people. Another reason: Roth’s concern about his own legacy. Now in his mid-70s, having exited retirement only after his handpicked successor left Vornado, he has little desire to gamble his career on a family and a property with uncertain futures, the people said.

Morali said Vornado and Kushner Cos. are equal partners in the tower and will jointly decide its fate.

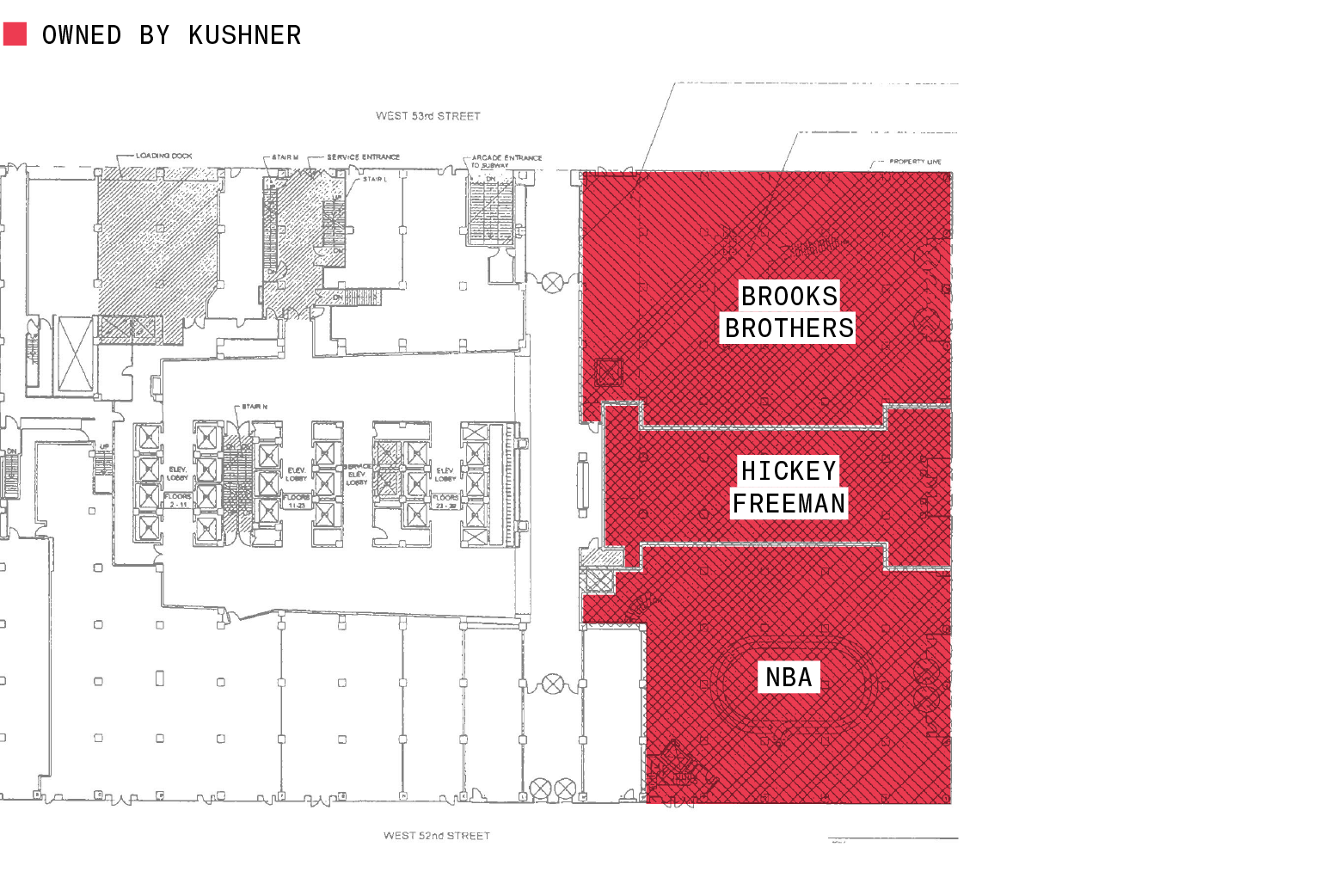

Gold on Fifth Avenue

Leasing and selling the building’s stores on the world’s most valuable shopping strip helped the Kushners dig themselves out of a deep hole.

The troubles caused by 666 Fifth have their origins in the overheated moment of its purchase. On Thanksgiving of 2006, Charlie Kushner made clear he wanted all employees in the office the next day. Tishman Speyer Properties, a real estate company with a New York pedigree his own company lacked, was looking to sell an office tower in midtown Manhattan, and Kushner wanted it. Tishman was demanding that the deal be done fast. The financing had to be put together by Sunday.

In retrospect, it would be difficult to imagine a worse time for the Kushners to have entered Manhattan real estate. Pension funds, insurers and other blue-chip firms wanted in on a market that many believed would climb forever, and landlords were loath to sell. The combination of new demand and limited supply created frenzy over each transaction, doubling prices.

Buying High

The Kushners didn’t have much cash on hand, weren’t in the habit of taking out 10-figure mortgages and weren’t very well known, so they needed an aggressive offer. Charlie Kushner’s dealmakers couldn’t get the numbers to add up, but he didn’t care. “I buy it, you make it work,” he told his accountants, according to a participant in the meeting.

A kingmaker in New Jersey Democratic politics, Kushner had been out of prison just three months for making illegal campaign contributions and, in a bizarre episode that the tabloids couldn’t get enough of, hiring a prostitute to entrap his brother-in-law. He wanted a prestige Manhattan property to mark a fresh start for the family business, which would now be led, if mostly in appearance, by his eldest child, Jared Kushner, who frequently consulted his father. Charlie had recently been turned down for towers including the Seagram Building. He saw securing Tishman’s property as a way to plant his flag.

Over the weekend, the Kushners and their partners worked out a deal in which they would put down $50 million—a pittance. Barclays Bank Plc and UBS Group AG funded $1.75 billion of the purchase, $535 million of it in short-term, high-interest loans. The terms were demanding, bordering on untenable. Nevertheless, after the deal closed in January 2007, the group celebrated with a party at one of the most expensive restaurants in New York, Per Se. Everyone there was given a pair of silver cufflinks fashioned in the embossed look of the building’s exterior.

High-stakes business mixed with politics and unwelcome publicity isn’t new to Jared Kushner. It characterized his initiation into the family firm. He was 23, just out of Harvard, when he was thrust into its leadership after his father went to prison.

Charlie and his three siblings had inherited a small real estate company from their parents, and under Charlie’s leadership, Kushner Cos. flourished. Over two decades, Charlie amassed about 25,000 middle- and working-class apartments, making him one of New Jersey’s largest landlords. Plain but lucrative, these massive suburban complexes threw off enough cash to fuel his political ambitions. As a major donor to the national Democratic Party, Charlie received visits from President Bill Clinton; he was also the single biggest financial backer of former New Jersey Governor Jim McGreevey, who appointed him to the board of the Port Authority of New York and New Jersey.

But Charlie used company money for his political donations, and his siblings didn’t care for it, leading to the infamous lawsuit and prosecution. Then-U.S. Attorney Chris Christie began a grand jury investigation.

The arrest and its coverage made Jared’s entry into the company hierarchy a crucible and strengthened his already fierce attachment to his father. During Charlie Kushner’s 14-month incarceration in an Alabama penitentiary, Jared flew down every Sunday. For years, he carried a wallet his dad had made him in the prison workshop. While his father was behind bars, Jared bought the New York Observer newspaper as a platform to reach the Manhattan elite and began pushing for the company to leave New Jersey behind. He ultimately set his sights on 666 Fifth.

At 1.5 million square feet, the 1950s building ranks nowhere near the largest of New York skyscrapers. Its low ceilings and closely built columns give it a dark, closed-off feel—anathema in the era of light-filled open-plan offices.

“If that building was beginning to look obsolete at the time of purchase, it is totally obsolete now,” says Jesse Keenan, a Harvard lecturer on architecture who wrote a 2013 report on the building for Kushner Cos. He notes that Manhattan is in the midst of its largest office-construction boom since the 1980s. The most prestigious occupants—hedge funds, private equity and law firms—are moving west to new buildings, shifting the center of gravity away from the Kushners.

As the building’s fate became increasingly bleak, the family, rather than forfeit, decided to go big. Their plan was to raze the structure and replace it with a glimmering Zaha Hadid-designed tower of massive proportions. The scale of the plan stirred the imagination, but the costs were astronomical because they involved repurchasing the property rights they’d sold to keep the original building afloat. That alone would require more than $1 billion. The elaborate renderings of the reconfigured building promised a kind of Time Warner Center on steroids: more than 80 stories with five levels of retail, a hotel and record-breaking expensive luxury condos on top.

For all its inspiring visuals, investors who reviewed the early version of the Kushners’ pitch book noticed a conspicuous omission: numbers. The company circulated a revised pitch, complete with financials, and the scale of the debt and risk involved were jarring. With a $4 billion construction loan and a business model that assumed the condos would sell at the aggressive price of $9,000 per square foot, it was similar to the leap of faith the Kushners had taken by overpaying for the original building a decade earlier, just before the boom went bust. A simple downturn in high-end New York real estate and the colossal new building would be in a hole of titanic proportions.

One early stop on the Kushners’ tour: Israel. Familiar with the country from their involvement in Jewish business ventures and philanthropy, they were able to partner with companies including Harel Insurance, Bank Leumi and Bank Hapoalim BM on various New York properties. But none invested in 666 Fifth.

Richard Goettlich, whom Charlie Kushner met in prison and hired, used his contacts to find others, former company employees say. In 2012, he approached Gaia, a firm connected to one of Israel’s wealthiest families, the Steinmetzes, whose fortune is derived from African diamonds. Gaia partnered with Kushner on a number of New York City buildings but not 666 Fifth. Goettlich didn’t respond to several requests for comment.

A pitch was made to Bernard Arnault, France’s richest man and the CEO of luxury-goods maker LVMH, to see if he might buy into the project’s multi-floor mall. He passed as well. A spokesman for Arnault declined to comment.

As 2015 drew to a close, there were no serious offers, and many in the company figured the plans were all but dead. Then Donald Trump began his meteoric political rise, and Jared Kushner was right on his coattails. Discussions heated up. Sheikh Hamad bin Jassim Al Thani, the Qatari businessman who had once run that nation’s sovereign-wealth fund, had earlier declined to even take a meeting with the Kushner Cos. executives, according to people familiar with the talks. In 2016, Al Thani agreed to invest $500 million from the private fund he runs, contingent on investment from others, which failed to materialize.

Also in 2016, Charlie and Jared met in New York with executives from the government-controlled South Korean sovereign fund asking for an investment in 666 Fifth. The Korea Investment Corporation didn’t invest, people familiar with the talks said.

The Kushners opened discussions with Anbang, the Chinese insurance giant with such close ties to the ruling party that the federal government has forbidden it from buying near a U.S. military base. During months of talks—before and after the election—Jared Kushner negotiated a proposal for Anbang to put billions into the building and allow the family firm to take away $400 million in cash. After details of that plan were made public in March, Anbang walked away amid a crackdown on foreign investments by Chinese regulators.

Representatives of Kushners Cos. also discussed the project with an executive working for Fawaz Alhokair, a Saudi billionaire whose company has vast holdings in shopping malls, hotels and real estate overseas. Alhokair made a splash in the U.S. when he paid $87.7 million for a Park Avenue penthouse. Alhokair’s company considered a possible investment in late 2015, according to Simon Marshall, who was CEO of Alhokair until this year.

Marshall said he analyzed the retail portion of the proposal. The building’s financial viability relied on a plan to construct five levels of luxury shopping at the base of a gleaming new tower. Marshall, who had overseen Alhokair’s retail operations around the world, said he found the projections to be more than the New York luxury-retail market would bear.

“The numbers just didn’t work,” Marshall said in a telephone interview, adding that politics played no role in the decision not to invest. The proposal remained on the table into late 2016, he said, as Trump continued on his path to the White House. Fawaz Alhokair didn’t respond to calls and emails for comment; Kushner Cos. also declined comment.

Staying in the Red

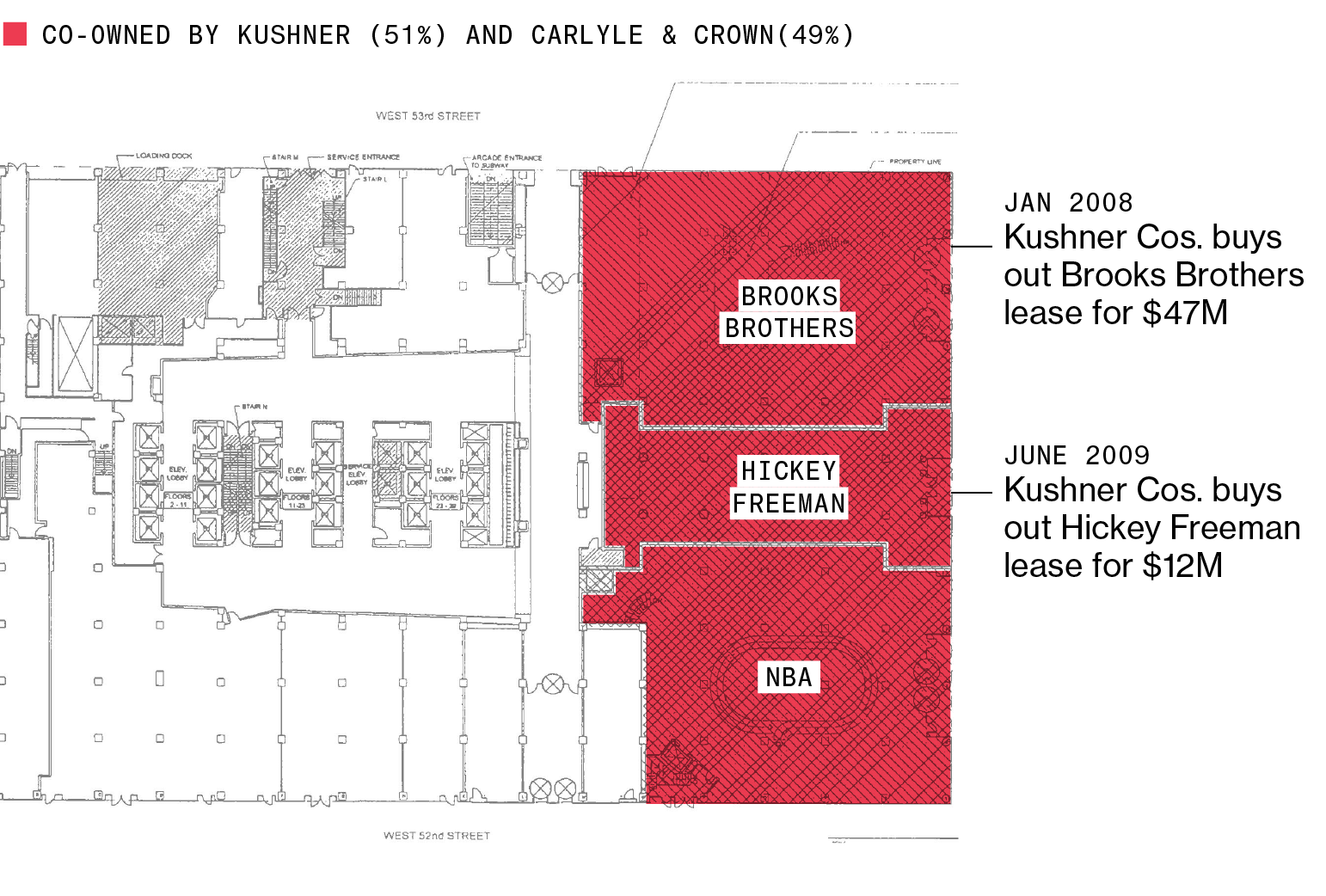

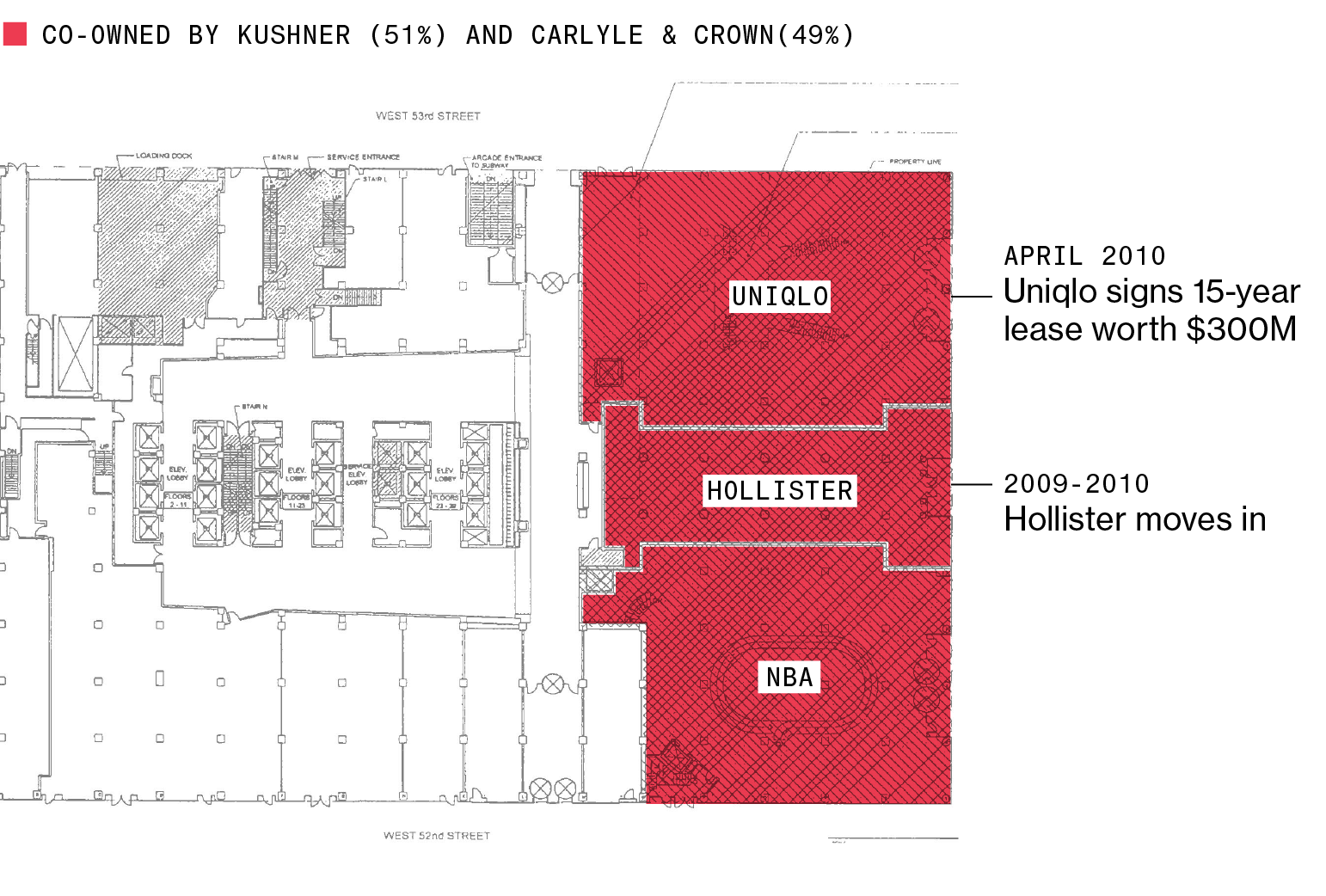

JAN 2007

The Kushners buy 666 Fifth for $1.8B, mostly with debt. Of that, $535M was in short-term, high interest loans.

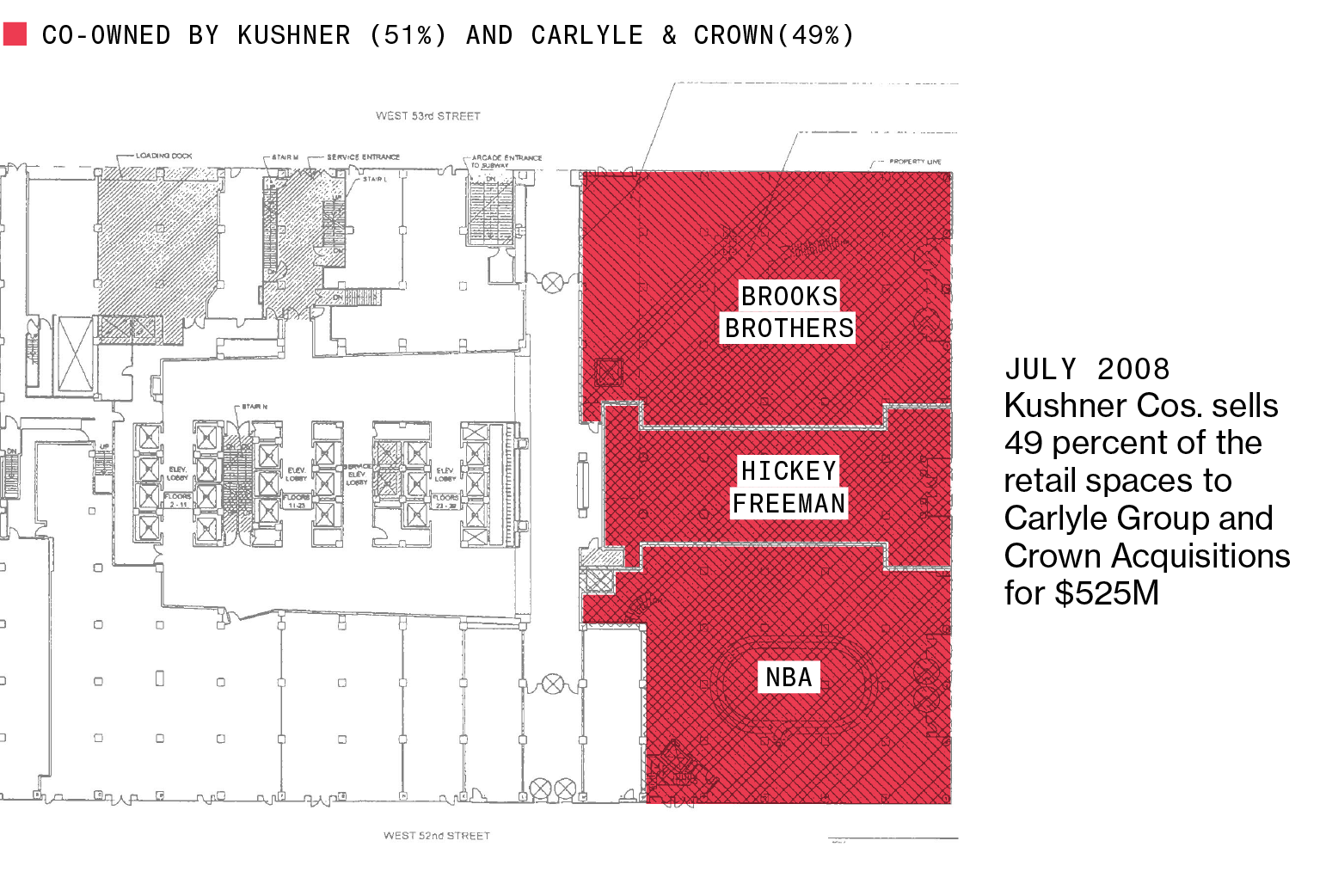

JULY 2008

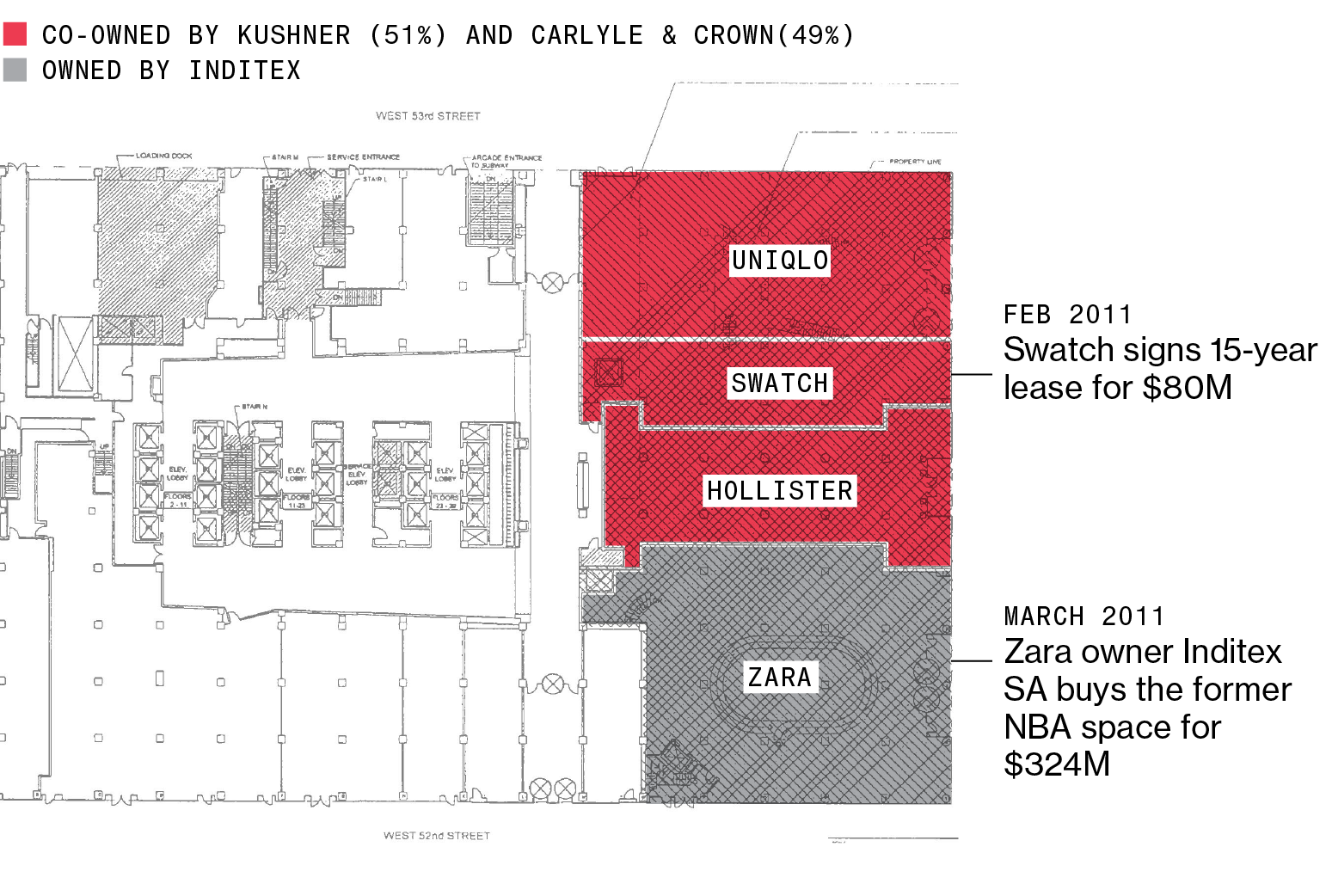

Kushner Cos. sells 49 percent of the retail spaces to Carlyle Group LP and Crown Acquisitions for $525M, and refinances the short-term debt.

MARCH 2011

The Kushner group sells one retail unit to Zara-owner Inditex SA for $324M.

2011

Vornado agrees to buy a 49.5 percent stake in the tower’s office spaces and adds $80 million of new equity. Kushner Cos. adds $30M. A portion of the principal loan—$115M—becomes a “hope note,” considered unlikely to be repaid.

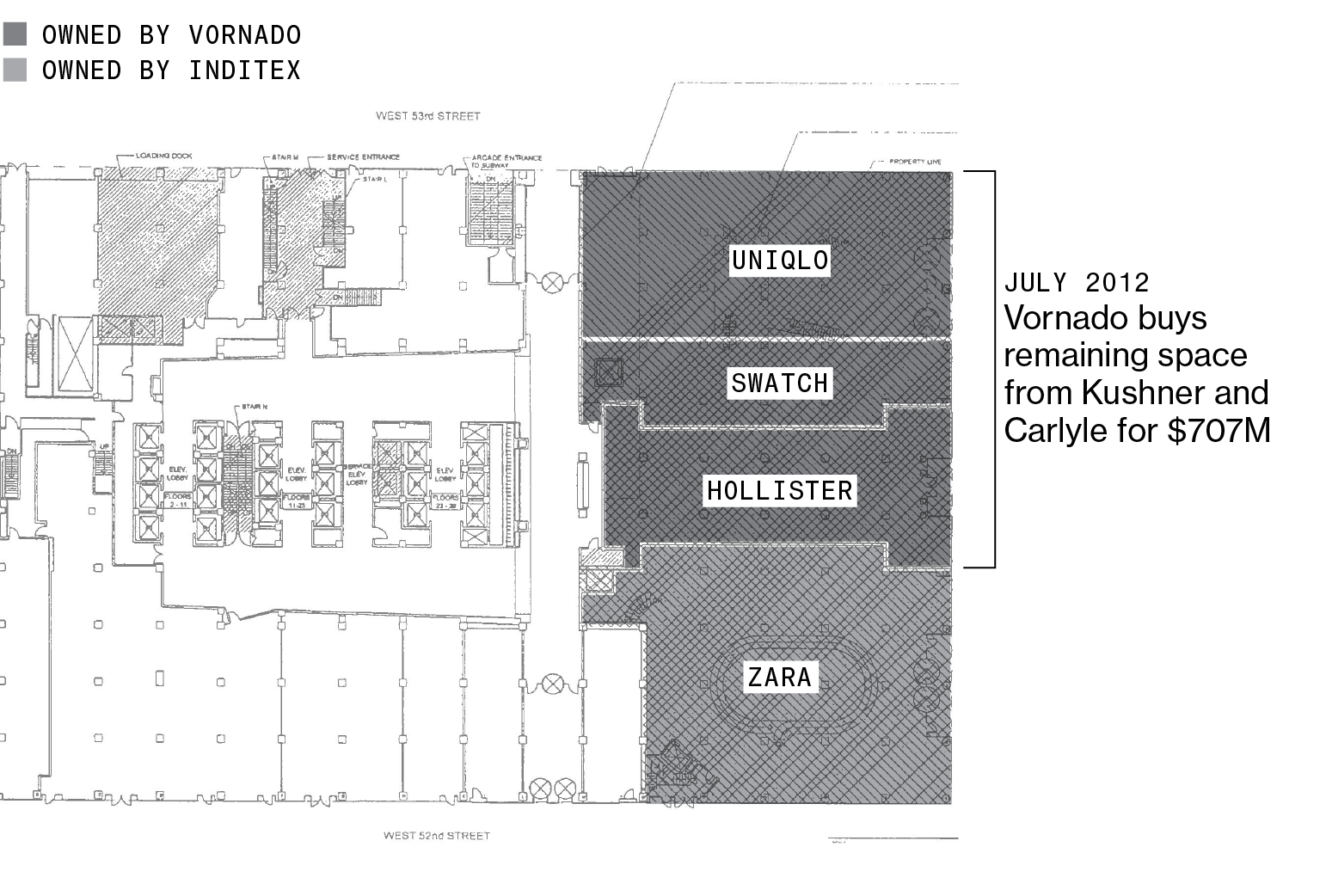

JULY 2012

Vornado agrees to buy remaining retail space from Kushner and Carlyle for $707M.

Even after all of these deals, the Kushners still haven’t touched the $1.1B principal.

Federal investigators know that Kushner met with then-Russian Ambassador Sergey Kislyak in Trump Tower last December and later met with Sergey Gorkov, head of the Kremlin-controlled VEB bank in two meetings that he didn’t, at first, disclose publicly or on his application for his national-security clearance. After those meetings became public, Kushner and the White House said the contacts were made in his role as a Trump adviser and didn’t involve discussion of his family business. But VEB and a spokesman for Russian President Vladimir Putin described the meetings quite differently, noted Adam Schiff of California, the top Democrat on the House Intelligence Committee. They said that Kushner was there in his capacity as head of his family’s real estate business. Investigators say they are studying those accounts with keen interest.

“I think it is part of a pattern of outreach to Russian financial interests, which are essentially Vladimir Putin and his oligarch circle, by Trump family members,” said Senator Richard Blumenthal of Connecticut, a Democrat on the Senate Judiciary Committee. “The financial dealings are important because we know that the Russian playbook is to engage and compromise foreign leaders.” He added, “Whether this meeting and contact are significant remains to be understood.” —With assistance from Billy House and Steven T. Dennis.

Tags: 666 Fifth, Carlyle & Crown, Chinese regulators, Crown Acquisitions, foreign investors, Inditex, Jared Kushner, Kremlin, Kushners properties, New York real estate, overseas fundraising, real estate business, Tishman Speyer Properties, Trump adviser '