Oxstones Investment Club™

Oxstones Investment Club™by Robert Huebscher, Advisor Perspectives,

Those Federal Reserve governors who intend to vote for an increase in rates at their December meeting need to take a close look at some of the charts Jeffrey Gundlach presented on Tuesday. One chart – which Gundlach called his “scariest” – carried a particularly ominous signal for the global economy.

Gundlach is the founder and chief investment officer of Los Angeles-based DoubleLine Capital. He spoke to investors via a conference call on November 17. Slides from that presentation are available here. The focus of his talk was DoubleLine’s asset-allocation mutual funds, DBLFX and DFLEX.

Gundlach reiterated what he has said in prior presentations: A rate increase is not a foregone conclusion, at least not until the December employment numbers are released, and he is not a strong supporter of an increase.

The weakness in the U.S. and global economies, as signaled by a number of charts, was the key new information in Gundlach’s presentation on Tuesday. He called the chart below “one of the scariest indicators in the world”:

The chart shows that nominal global GDP growth on a dollar-denominated basis is -5.0% on a year-over-year basis. It was this low only twice, in 2009 and 1982, he said. Coincidentally, the Fed raised rates in 1982, which was one of only two times it did so when nominal GDP in the U.S. was below 4.2%.

I’ll show some of the other slides that Gundlach called worrisome, but first let’s look at his comments on Fed policy and the economy.

The economy and the Fed

The implied probability of a rate increase in December, based on the market pricing, is 64%, according to Gundlach. “That seems just about right,” he said. If the employment data is similar or better, the Fed will raise rates, he said; if data is worse, they won’t. That means that two out of three scenarios favor a rate increase, consistent with the market’s 64% probability.

That probability is also consistent with the stated positions of the Fed governors, he said.

“The final outcome will be highly dependent on not just the economy,” said Gundlach, “but also the credit markets.” Gundlach said that many sectors of the credit and commodity markets are “falling apart.”

Unless the data starts to improve, he said the Fed may reverse an eventual rate increase, as has been the case in Sweden and several other countries.

Gundlach said he was struck by the divergence of policies in the U.S. and Europe. In the U.S., real GDP is growing at 2%, and in the E.U. it is 1.5%. The 50 basis points difference does not align with the aggressively expansive policy in Europe and the calls for Fed tightening in the U.S., he said, even though unemployment rates are much higher in Europe.

“These are not great economic growth rates anyway,” he said.

There is something of an “industrial recession” going on in the U.S., Gundlach said. Industrial production year-over-year is “already in recessionary conditions,” and is near zero.

The core CPI is 1.9%, only 0.1% away from the Fed’s target. The problem, he said, is that the PCE (the Fed’s preferred indicator) has been running below that for some time. The PCE is moving lower or possibility stabilizing, he said. Headline CPI is 0.2%, due to cheap energy and commodities, and is consistent with PriceStats (an internet-based indicator that is updated daily).

If the U.S. CPI was calculated the same way as in Europe, our CPI would be in deflation, according to Gundlach. That underscores the difference in monetary policies in the U.S. in Europe; the situations in the two are “not really different,” he said, and don’t call for radically different policies.

The Fed backed off from a possible rate increase earlier this year, citing the strength of the dollar. Now the dollar is rallying again, Gundlach said. It closed at 99.6 on the DXY. If it closes twice above the March high of 100.3, it will “break out to the upside,” he said, and the Fed would not raise interest rates.

There is over $9 trillion in dollar-denominated debt outside the U.S., which will be problematic if the dollar continues to increase, according to Gundlach. So far, there isn’t a crisis condition. But if there is “another dollar leg up,” he said he would be talking about a debt crisis in future webcasts. That would be bad for commodities, U.S. exports and earnings.

Commodity prices have been weak, and the CRB is below the depths it reached during the financial crisis and is at a 13-year low. Most of this is due to economic weakness globally, especially in China, he said. The dollar will be influenced by China, according to Gundlach. If the Fed hikes rates and China continues to slow down, then he said the dollar will get a lot stronger.

The stock market is the indicator that the Fed “pretends it doesn’t look at,” Gundlach said. The 12-month trailing S&P earnings are now going “dead sideways” to slightly lower, he said. “The real question mark is whether earnings will go up in 2016, but that is not likely if the dollar stays higher,” he said.

To predict earnings, Gundlach said, “If you want to be depressed and lose a lot of sleep, look at this chart of profit margins”:

The current downward trend in margins is almost perfectly consistent with the onset of prior recessions, according to Gundlach.

He said this was “the most bearish chart for the U.S. economy.” Gundlach said that analysts make a lot of “caveats” about “carving out certain data” to justify higher earnings. In response, he said that if you ask DoubleLine for a portfolio review and you “leave out the stuff that’s down, we’ll give you a happy report.”

Relative value across the bond market

Gundlach discussed the relative valuation of various sectors in the bond market.

Agency mortgage-backed securities are “nearly exactly fairly valued,” he said. He advocated having a market weight to those securities.

Commercial mortgage-backed securities (CMBS) are priced “a little bit rich,” he said. But using other methodologies showed that they were cheap.

Entering 2014, investment-grade corporate bonds were extremely rich. Now they are overvalued, he said, but not as badly as at the beginning of the year.

He compares high-yield bonds to long-dated Treasury bonds because they have similar volatilities. They were at their most overvalued at the end of 2013. Now, he said, they are overvalued to the same degree as investment-grade bonds. The number of junk bond downgrades just crossed over and now exceeds the number of upgrades, he said; the reverse was true for most of the last five years.

For those who say they should hold their energy bonds in anticipation of oil prices increasing to $70, Gundlach had a recommendation: Sell the bonds and buy oil. The reason he gave was that energy bonds will fare very poorly if oil remains at its current price or decreases in price. Under those conditions, however, oil as a commodity would do relatively better.

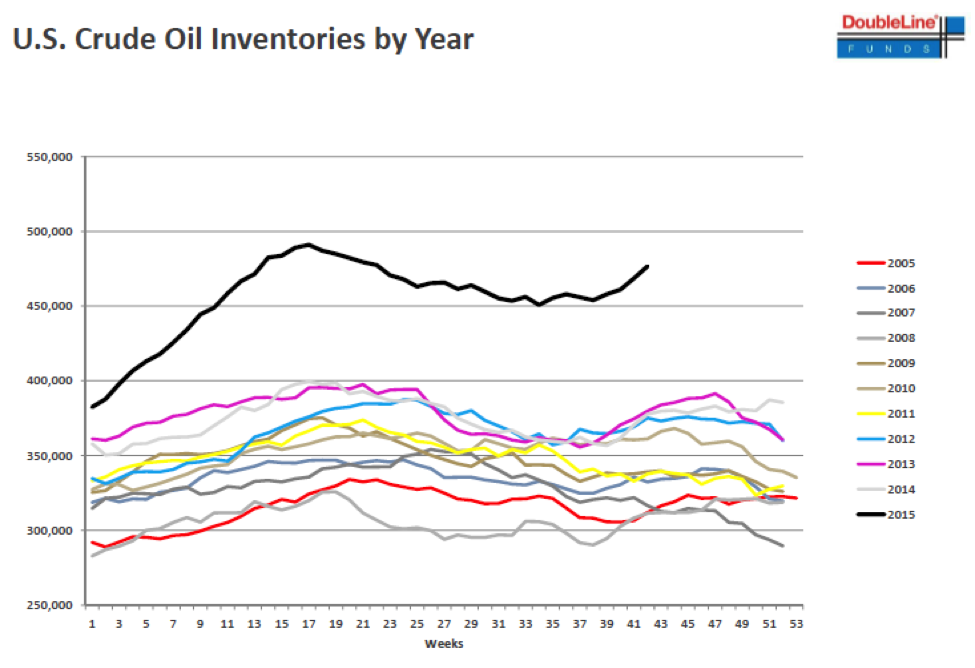

The junk bond market needs higher oil prices, he said, not just stable prices. To assess the potential for higher oil prices, here is what he called “the chart of the day”:

This chart shows how much higher oil inventories are in 2015 versus the prior decade. “I don’t see how anyone can make a fundamental argument for oil going higher with this fact in play,” he said.

He believes consumer-related debt is good to own but advises avoiding anything that is exposed to the commodity cycles.

Municipal bonds, he said, were a “little rich.” Gundlach said Illinois bonds were dangerous and investors were “playing a game of beat the clock” before those bonds are downgraded.

There is no reason to believe TIPS will outperform nominal bonds, he said, but they are not the best inflation hedge. For that, he recommended buying oil.

Emerging-market dollar-denominated bonds were a “little bit cheap,” he said. If the dollar stays controlled (the DXY below 100), Gundlach believes that emerging-market bonds would be the best-performing sector in the fixed income markets. He said that if emerging-markets bonds do well, investors would be fine in dollar-denominate bonds and it would not be necessary to hold local-currency bonds.

Bank loans are priced at the “rich end,” he said. If commodity prices fail to increase, they will deteriorate along with junk bonds. The JP Morgan index of the 100 most liquid bank loans has declined precipitously since May.

Spreads are widening on corporate bonds, he said, in the investment-grade and junk sectors. Taken against a generally rising interest rate environment, Gundlach questioned whether investors should have any exposure in those markets.

“You have a double whammy affecting the corporate economy,” he said. “How can that be good? Why would you want exposure to those sectors if the Fed is intent on raising interest rates against a very weak backdrop of mixed econ indicators? What’s coming out of the junk bond market is the loudest cry that one can find about why the Fed is reluctant to raise interest rates.”

http://www.advisorperspectives.com/articles/2015/11/19/gundlach-the-scariest-indicator-in-the-world/4

Tags: 60bp decline in net profit margins usually consistent with the onset of prior recessions, agency mortgage backed bonds, asset allocations, bank loans, bond asset classes, bond valuations, china slowdown, CMBS, commodities, commodity cycles, CPI, deflation, diverging monetary policies in U.S. and EU, dollar-denominated debt outside the U.S. is a growing problem, DoubleLine, economic charts, economic indicator, Economic Trends, emerging market bonds are undervalued, global nominal gdp, high yield bonds, Industrial production is in recessionary conditions, investment grade bonds, investment wisdom, Jeffrey Gundlach, junk bonds, large overhang of oil inventories, lower oil prices, macroeconomics, monetary policy, muni bonds, nominal global GDP growth on a dollar-denominated basis is -5.0%, oil, pce, recession indicators, recession predictors, strong dollar creating a global crisis, the most bearish chart on the U.S. economy is the 60bps decline in net profit margins, tips, U.S. economy