Oxstones Investment Club™

Oxstones Investment Club™By Eddie Chow, From Mark Mobius Blog,

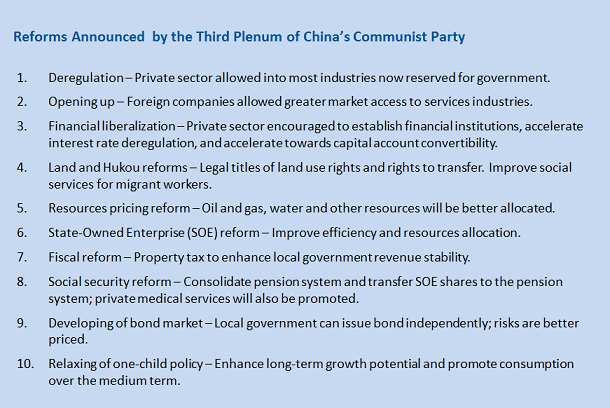

Reform efforts in China seem to be gaining momentum. The big question is whether these reforms will buoy investor confidence, and jumpstart China’s local A-share market. In November 2013, the Chinese Communist Party convened its Third Plenary Session, resulting in a general blueprint for the country going forward officially called “A Decision on Major Issues Concerning Comprehensive and Far-Reaching Reforms.” There were a variety of areas targeted, including fiscal reform, anti-corruption efforts, and integrated rural-urban development. Since then, the Chinese government has released more detailed reforms plans, and of particular interest to us as investors are those related to the capital markets. I’ve invited my colleague Eddie Chow, senior executive vice president and managing director, Templeton Emerging Markets Group, to share his perspective on these reform efforts and his outlook for China’s equity market.

Eddie Chow

Eddie ChowEddie Chow

Senior Executive Vice President and Managing Director

Templeton Emerging Markets Group

The Chinese government, through both the communications during the National Peoples’ Congress in March and more recently in the release of the “Guiding Principles for the Healthy Development of Capital Markets” by the State Council, has put up a detailed agenda for capital market reform. The reform plan is comprehensive and we believe most of the specific reforms initiated are significant for investors. Some of them could have an immediate impact, while some are more structural in nature, rendering potential market impact over a longer-term basis. For example, on the opening up of the capital markets, the Shanghai–Hong Kong Stock Connect Scheme, which increases both inward and outward investment quotas and relaxes foreign shareholder limits in listed companies, could very soon help inject more liquidity into the local China A-share market. Over the medium to longer term, we believe the greater participation of foreign investors may change behaviors and dynamics of the market and even governance at the company level. To improve the structure of the capital markets, in addition to developing the bond market (which itself is essential in helping to determine prices for costs of capital in China), the approval-based stock issuance system in the A-share market will be replaced with a registration-based one. There are also new rules governing initial public offerings (IPOs) published by the Securities Association of China. Additionally, we believe regulators will work to crack down on potential insider trading, enhance information disclosure, improve delisting regime and support pension fund investments. We also believe all these new reform initiatives should help gradually regain interest in China’s A-share market.The goal of these efforts is to make China’s capital markets much more diverse, structured and transparent. This is very important, in our view, as there is a large amount of private savings in China that could be invested. So far, much of the work is being done by the state-owned dominated banking system and of course, the banking system has a lot of limitations.

The Reality of Implementing Reforms

The Reality of Implementing Reforms

Overall, China’s domestic equity market was quite weak in the first half of 2014 for a host of reasons. The market has been negatively impacted by weak macroeconomic data, worries on news of bond defaults and rising new share supply in the equity market. Although reform excitement had lifted the longer-term structural outlook of the economy and the market late last year, the China A-share market started to correct after the Third Plenum ended. Attention subsequently turned to the reality of implementing reforms.

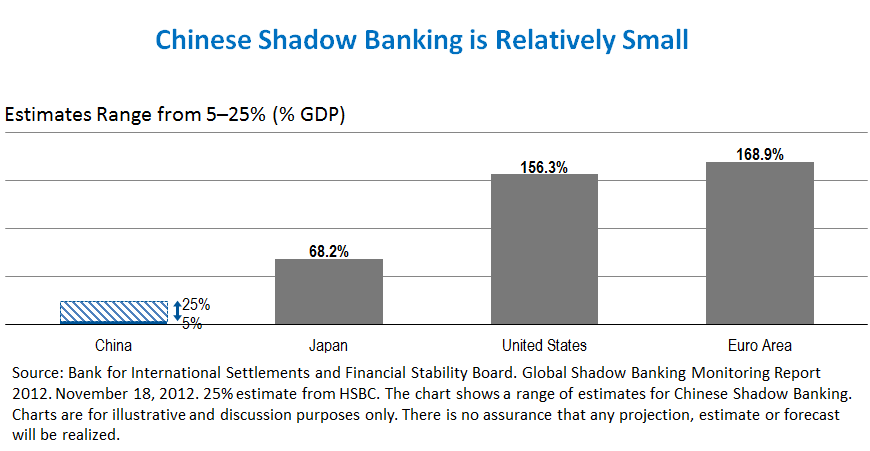

Moreover, we believe that the economy has to be able to bear growing at a slower pace in order for it to rebalance from its heavy reliance on investments. In our view, monetary policies and credit growth cannot be tilted toward loosening if the government wants to fix the underlying situation of over-leverage in the economy. There could likely be more bond defaults, and property prices may likely have to come down for the growth of shadow banking activities to be curbed. There are signs that the property market could be undergoing an adjustment. A pullback in prices wouldn’t concern us too much, as we believe this could benefit the longer-term development of the property market by taking out some excess investments and redirecting some capital to other sectors. The press often presents shadow banking (financial intermediaries generally outside of regulatory oversight) in a negative light, but in some ways it could be considered a form of liberalization of the interest rate market in China and a complement to the banking sector.Companies that cannot borrow at the designated low benchmark rates have been able to borrow at higher rates, while depositors who do not accept the low benchmark deposit rates can take higher risk and go into higher risk assets. The key, we think, is whether the risks are properly priced and are known by asset holders. China’s shadow banking activities, relative to the size of the economy, are not excessive in our view. The problem, as we see it, is that activity has grown too fast and much was directed to the property, mining and metal trading activities of the Chinese economy that are facing strong cyclical headwinds. Tighter regulations and more disclosure requirements are gradually being put in place, so we do not think shadow banking will pose a major threat to China’s overall banking system.

Markets in Japan and India experienced sharp rallies in the wake of their own reform announcements and initiatives, and so far, we haven’t seen that level of excitement reflected in China’s market. However, we think the backdrop for those markets and the kinds of reforms Japan and India are talking about are very different from the situation in China. Japan’s economy was marred by threats of deflation, so when Japan’s Prime Minister Shinzo Abe talked about economic reforms using the “three arrows” (fiscal stimulus, monetary easing and structural reform), the market to a great degree reacted to the second arrow, i.e. monetary easing. The proposed easing in Japan, with a 2% inflation target specified, is clearly inflationary and unprecedented, and by scale, if one measures it against the size of the economy, is even larger than the quantitative easing that was done by the US Federal Reserve. In China, there was very little reform action on the monetary front.

In India, the victory of the BJP-led alliance and winning with a simple majority as it did in Parliament was a watershed event in the country’s history. This suggests the country should have a strong government able to uphold crucial legislations that put forth reforms that were basically non-existent over the past few decades. The market has high hopes that the new government can address the structural problems of weak fiscal discipline, too much rural subsidies and not enough infrastructure spending. Compared with China, India has a relatively better demographic backdrop, less global participation and relatively better cyclical condition, with excess already contracted by higher interest rates and current account deficits narrowed by currency adjustment. The winning of the BJP gave the market and economy a lot of room for potential upward adjustment, in our view.

In China, although President Xi and Premier Li are trying to tackle structural issues that were created by the excessive credit supply to the state-owned sector after the global financial crisis, the reforms, in the context of how much the direction of policies is going to change, appear much less drastic than in India.

Restoring Investor Confidence in China

To restore investor confidence, or to see structurally higher valuation multiples for the market, we would need to see the market itself execute its role of effectively and efficiently intermediating capital. We think investors’ confidence will likely return when they perceive the following is to occur:

- Companies can be listed and raise additional capital without hindrance from excessive bureaucracies

- Poorly managed companies can be delisted or bought by better companies under proper market rulings

- Minority shareholder rights are well-protected

- Management and major shareholders are well-governed

We believe China’s comprehensive capital market reform plan is the right step taken by the government, but the market still doesn’t seem too confident the government is willing to take the short-term pain to put all these reform proposals into action. For example, some companies have been waiting for years to be listed, but the China Securities Regulatory Commission’s (CSRC) approval process for IPOs is still slow, likely because of a fear that excess supply could negatively impact the market. Structurally, risks in the corporate bond market and on many trust loans are not priced in, in our view. Many bond holders still appear to be subscribing to the view that no matter how bad the issuers’ financial condition is, expired bonds will easily be refinanced and won’t come into default. Ironically, we believe more bond defaults, which lead to risks more appropriately priced, could help push some flows back to equities and could be beneficial for the China A-share market.

China: The Investment Case

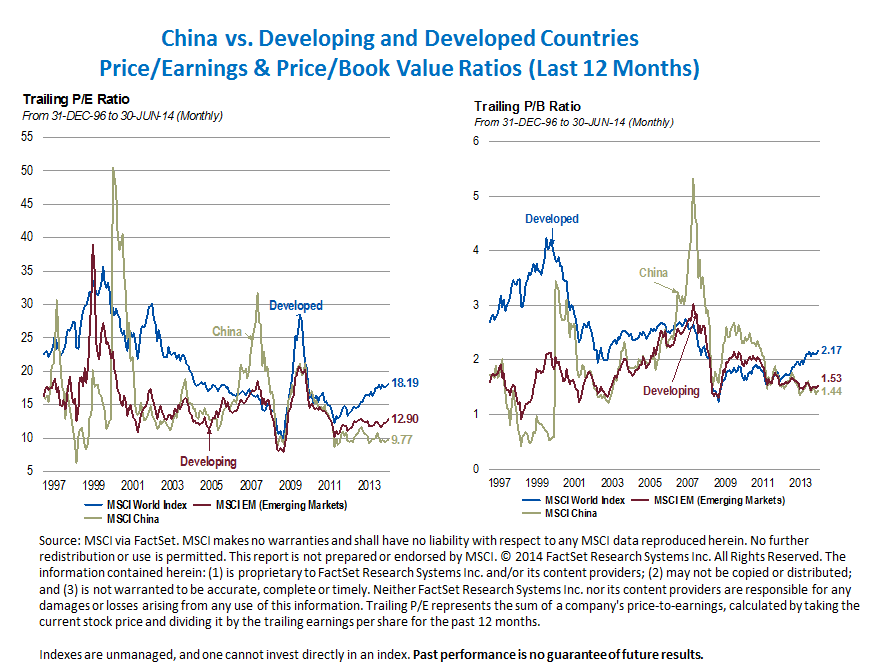

While China represents one of the largest economies in the world, it is a typical emerging market in that it still has a relatively low participation of institutional and foreign investors. This provides good potential opportunities for value- oriented investors like us, as valuations have generally been depressed by the lack of market confidence. We believe the lack of confidence is transitional and the capital market reform initiatives show that the government wants to address this issue.

We have found good values in banks in particular, mainly the larger banks with stronger deposit franchises, and in some other financial companies that have the potential to benefit from the development of capital markets. We also see good long-term value in the building materials sector, which has undergone massive market consolidation and capacity rationalization. Underpinned by structural demand growth we also positively view pharmaceutical and selected companies in the consumer sector in China.

Mark Mobius’s and Eddie Chow’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Tags: Asia, China, chinese banking system, chinese financial liberalization, chinese government policies, chinese land and hukou reforms, chinese market reforms, chinese social policy reforms, Chinese stock market, chinese stock market fundamentals, chinese stock market valuation, developing chinese municipal bond market, emerging markets, implementing market reforms in china, India BJP election win, Japan economic reforms, private sector deregulation in china, rebalancing the chinese economy, relax the one child policy, SOE reforms in China, value investing