Oxstones Investment Club™

Oxstones Investment Club™By Mark Mobius, Franklin Templeton,

Southeast Asia represents one of the fastest-growing regions of the world today, and to us, its future looks bright, despite some ups and downs. Overall, we believe there is much to be positive about as long-term investors in Southeast Asia, including regional cooperation that could create additional investment opportunities.

The Association of Southeast Asian Nations (ASEAN) was founded in 1967 with five member countries: Indonesia, Malaysia, the Philippines, Singapore and Thailand. Today, there are 10 members, which include the burgeoning frontier market of Myanmar, which recently hosted the 24th ASEAN Summit. ASEAN granted Myanmar (also known as Burma) regional membership in 1997, and subsequent dialogue and pressure from ASEAN played a large part in opening up what was, at that time, an isolated country, inspiring positive political and economic change there. During the 2008 Cyclone Nargis disaster, for example, ASEAN managed to persuade Myanmar’s government to allow foreign humanitarian aid in to help its citizens. At its onset, ASEAN outlined its aims as accelerating economic growth, social progress and cultural development among its members, as well as promoting regional peace.

The ASEAN Economic Community (AEC) is expected to come to fruition in 2015, although some say the deadline might be a little ambitious. It represents a common market that is expected to comprise 600 million people and have a combined GDP of nearly US$2 trillion.1 The AEC is envisaged to have the following key characteristics: (a) a single market and production base, (b) a highly competitive economic region, (c) a region of equitable economic development and (d) a region fully integrated into the global economy.2 Of course, there are enormous challenges involved in harmonizing financial and economic integration and making necessary reforms, including cultural and political differences, but I think these challenges can be overcome.

We think the formation of this economic community is quite exciting, representing a regional bloc akin to the eurozone. It should enable companies to establish plants in any of the ASEAN nations and easily access these markets. Parts produced in different countries should be able to be transported across borders with few restrictions or taxes so that production efficiencies can be achieved. The successful formation of the European Union provides a blueprint for ASEAN and also enables the ASEAN nations to learn from some of the problems that the Europeans have faced. I think the ASEAN free trade area could potentially offer a market equal in influence to China in the long term in some regards, and increased regional trade could help lessen dependence on both the United States and China. Compared with markets like the United States or China, individual ASEAN member markets look small and less liquid, but by coming together, the region could become a much larger market force and global power, too, something China is keenly aware of, particularly in light of recent territorial disputes in the South China Sea.

I think ASEAN could be a counterweight to China and make its voice known in a unified way to the world. The formation of the AEC could also drive more investor flows to the region going forward, in addition to liquidity fueled by Japan’s ambitious “Abenomics” program.

As bottom-up investors, we continue to look at individual investment opportunities in individual countries on a case-by-case basis. Here are some of my thoughts and those of my team regarding the outlook and developments in the Philippines, Thailand, Indonesia, Malaysia and Vietnam, and potential investment opportunities we see.

Philippines

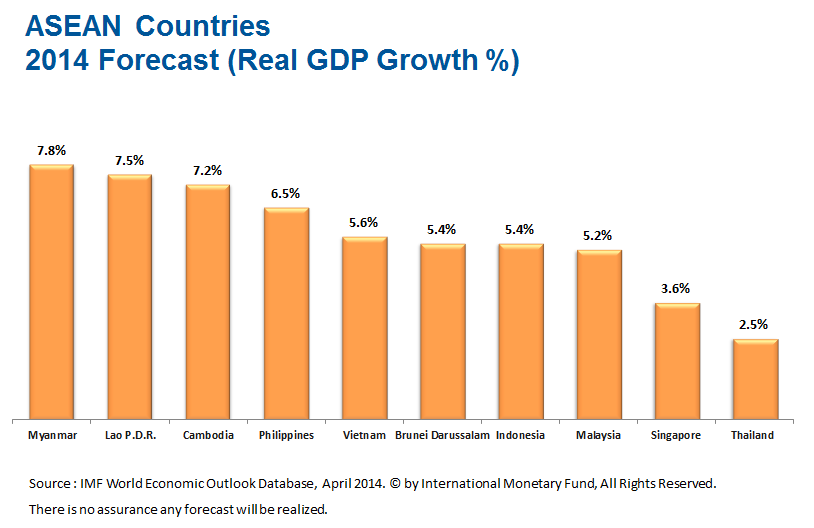

The future appears to be looking brighter for the Philippines, the host of the World Economic Forum on East Asia in May, as it recovers from the devastation of Typhoon Haiyan in November 2013. The Philippines looks to remain a key contributor to growth in the region this year and next (6.5% GDP growth is forecast in 2014 and 20153), and its local stock market has reflected investor optimism so far this year. Of course, the country still faces challenges in its rebuilding efforts, but seems to be bouncing back. Economic data there have been looking good recently, and ratings agency Standard & Poor’s4 recently raised the Philippines’s credit score to BBB, or two notches above investment grade, citing improvements in structural, administrative, institutional and governance reforms.

The future appears to be looking brighter for the Philippines, the host of the World Economic Forum on East Asia in May, as it recovers from the devastation of Typhoon Haiyan in November 2013. The Philippines looks to remain a key contributor to growth in the region this year and next (6.5% GDP growth is forecast in 2014 and 20153), and its local stock market has reflected investor optimism so far this year. Of course, the country still faces challenges in its rebuilding efforts, but seems to be bouncing back. Economic data there have been looking good recently, and ratings agency Standard & Poor’s4 recently raised the Philippines’s credit score to BBB, or two notches above investment grade, citing improvements in structural, administrative, institutional and governance reforms.

Thailand

We’ve been investing in Thailand for a long time and have been through lots of ups and downs. Recently, political tensions have again flared after Thailand’s Constitutional Court dismissed Prime Minister Yingluck Shinawatra, ruling she had violated the constitution. We believe there will be continuing uncertainty in Thailand that could keep many investors at bay until there is more clarity and stability in the political environment. Tourism could likewise be affected if tensions continue to escalate. Nevertheless, we don’t believe existing company operations are likely to be greatly interrupted, and we would view a potential decline in the Thai stock market as an opportunity to look for selective bargains there. Many Thai corporations have managed to weather various bouts of political upheaval and even thrive in spite of them, proving the strength and resilience of the Thai people.

The long-term prognosis for Thailand is positive, in our view, given that direct foreign investors want stability in the country. The reality of the situation as we see it is that an elective government seems difficult to achieve today, but our Templeton Emerging Markets Group will continue to wait and see which government is installed next. Certain company stocks may take a temporary dip, but nevertheless, we don’t believe existing company operations will be interrupted.

From a long-range view, we think many companies will be able to survive and prosper in Thailand. Thailand is going through the throes of an incredible class conflict right now between the rich and the poor, and neither side seems to want to back down. We do believe cooler heads should prevail over time, and the more positive economic trends Thailand has seen could revert, including rising per-capita incomes. Thailand has a large middle class and a growing consumer population, which bodes well for the economy going forward. As investors, we have been focusing on consumer goods and services, including banks and property companies, as people move to the cities and require housing.

Indonesia

Improving economic data flow, optimism that elections would produce a reformist government, and some encouraging amendments to a proposed ban on metal ore exports all boosted investor sentiment in Indonesia this year, strengthening both its share market and its currency, the rupiah. Indonesia benefits from tremendous natural resources—a large nickel producer, it is a key supplier for the Chinese stainless steel industry in particular. Indonesia’s government is forcing the natural resources sector to move downstream from manufacturing to finished products. It unveiled a sweeping ban on mineral exports aimed at boosting Indonesia’s profits from its mineral wealth by forcing miners to process their ores before export. However, this shift comes at a significant financial cost for mining companies there, and the ban is likely to result in at least a short-term reduction in foreign revenue. However, longer term, we believe this change means the industrial sector should grow. Indonesia provides an example of how ASEAN nations are becoming a growing force politically and economically because they are tearing down barriers to trade.

Indonesia has really seen a political transformation in recent years with an incredible effort to centralize power in Jakarta. It had to be done, because Indonesia is a collection of islands with lots of tribal differences and interests. It was a lot of work to pull the nation together. Under the recent administration, however, more regionalization was allowed: Provinces were given more power because the government realized it was impossible to direct from the center given all the differences. Although divesting some power to the provinces initially resulted in a rise in corruption at the local level, it also led to a lot of progress made at the local level. Today, people are very aware of corruption and are angry about it, which has created a reform movement. If Indonesia can go even part of the way toward alleviating corruption at every level, we think this would be positive for investors.

Similar to Thailand, Indonesia has a growing middle class, and as investors there, we have been favoring consumer-oriented investment themes there, including banking and automobiles. We recognize that Indonesia is a unique market in many ways. For example, the most popular mobile phone in Indonesia in recent years has been the BlackBerry, which may surprise a lot of people. That’s why we think it’s so important to have a local presence, to do on-the-ground research and know each market intimately.

Malaysia

We think Malaysia has made great strides recently by increasing transparency in government. In addition, Malaysia’s government has been taking measures to reduce subsidies, including subsidies on sugar and fuel. We think this is a sound policy initiative that could pay off for Malaysia in the long run, because budget deficits could be minimized and the economy could be put on a more realistic and firmer footing. Certain subsidies can be very popular with the people, so it’s difficult for politicians to reduce them. However, we think if Malaysia’s politicians can take the lead in this regard, it could be positive for the economy in the long term. Some say Malaysia’s civil service sector is quite bloated, accounting for a significant portion of its GDP. Politicians have been more forthright in making the government more efficient. They’ve raised bonuses and salaries for government employees, which could be positive but we think only makes sense if it results in better quality and more efficient employees. More important, I think, is the need for privatization of many of the country’s activities that are now undertaken by the government. This is a trend that is global in nature and that we are seeing more and more as we travel to different emerging markets around the world—more privatization is taking place. When the burden on the government is less, it can reduce its workforce and transfer more workers to the private sector. But more importantly, with privatization generally comes a more efficient delivery of services to the people.

Like other countries in the region, consumer spending power has been on the rise in Malaysia, which has become one of the world’s largest luxury goods markets. A combination of accelerating economic growth and population growth is increasing overall consumption, and the country has benefited from an influx of wealthy tourists eager to explore its designer shops.

Vietnam

Vietnam is an example of a previously underdeveloped country that is starting to see significant catch-up growth as it transitions from a communist society to a capitalist or market-oriented society, benefiting from normalized relations with the United States and membership in the World Trade Organization.

The country has been growing at a fast pace, with annual GDP growth from 2000 –2013 averaging 6.5%.5 Vietnam’s growth has been broad-based and fueled by both rising domestic demand and globally competitive exports. The manufacturing sector has been particularly robust, growing at a 9.3% annual compounded growth rate from 2005 to 2010, encompassing a range of products from automobiles to clothing.6 Additionally, some multinational companies have been adding a second or third base of production in Vietnam, as part of a “China plus one” strategy, to take advantage of Vietnam’s cost advantages.

We have found that Vietnam benefits from a very hardworking, smart population, and we believe the potential investment opportunities in the country are likely to expand as its market continues to develop. There are many companies there that represent good values, in our view, and the management of many Vietnamese companies appears to be quite good as well.

In general, high economic growth rates in many Southeast Asian countries—driven by favorable demographics, ongoing urbanization, rapid productivity gains and improving technology—are underpinned in many cases by solid finances. We believe the potential for Asian economic growth to feed into corporate profitability is not fully recognized in many cases, so we remain on the lookout for potential opportunities to invest at favorable prices in the region.

Dr. Mobius’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

All investments involve risks, including possible loss of principal. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Currency rates may fluctuate significantly over short periods of time and can reduce returns.

3. Source: IMF World Economic Outlook Database, April 2014. © by International Monetary Fund. All Rights Reserved.

4. Source: Standard & Poor’s. This may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard & Poor’s. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell products. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on as investment advice.

Tags: AEC, ASEAN, ASEAN Economic Community, asian regional trade bloc, asian tiger economy, Association of Southeast Asian Nations, China, emerging economies, fastest growing economies, Indonesia, malaysia, Myanmar, philippines, singapore, South China Sea, southeast asia, southeast asia free trade zone, thailand